Behind the Desk: A Day in the Life of an Insurance Agency Owner

It's 7:15 AM on a Tuesday, and Michael, an insurance agency owner, hasn't even made it to his desk yet.

His phone is already lighting up. A producer needs approval on a non-standard risk, the carrier rep moved this morning's meeting, and a long-time client just forwarded an email with "URGENT" in the subject line.

Michael had blocked out today for strategic planning. He wanted to finally analyze which lines of business are actually profitable, review that expansion opportunity in the next county, and maybe—just maybe—make some calls to that list of prospects gathering dust on his desk.

By 9 AM, those plans will be completely derailed.

This is what life looks like for many insurance agency owners today. The job demands leadership and strategy, but the day-to-day reality is often dominated by manual work, urgent requests, and decisions that can’t wait.

Below, we’ll break down what an insurance agency owner actually does, what a typical day really looks like behind the scenes, and how modern tools are reshaping the role, freeing owners up to focus on growth, leadership, and the work that truly moves the agency forward.

What Does an Insurance Agency Owner Actually Do?

An insurance agency owner wears a lot of hats—often more than they should.

Depending on the size and structure of the agency, owners are responsible for setting growth targets, managing carrier relationships, overseeing producers and account managers, handling major client escalations, and making strategic decisions about markets, staffing, and profitability.

In theory, the job is strategic.

In practice, many insurance agency owners find themselves pulled deep into operational work—reviewing complex renewals, analyzing loss runs, answering coverage questions, and filling gaps when the team is overwhelmed.

Michael’s day is a perfect example.

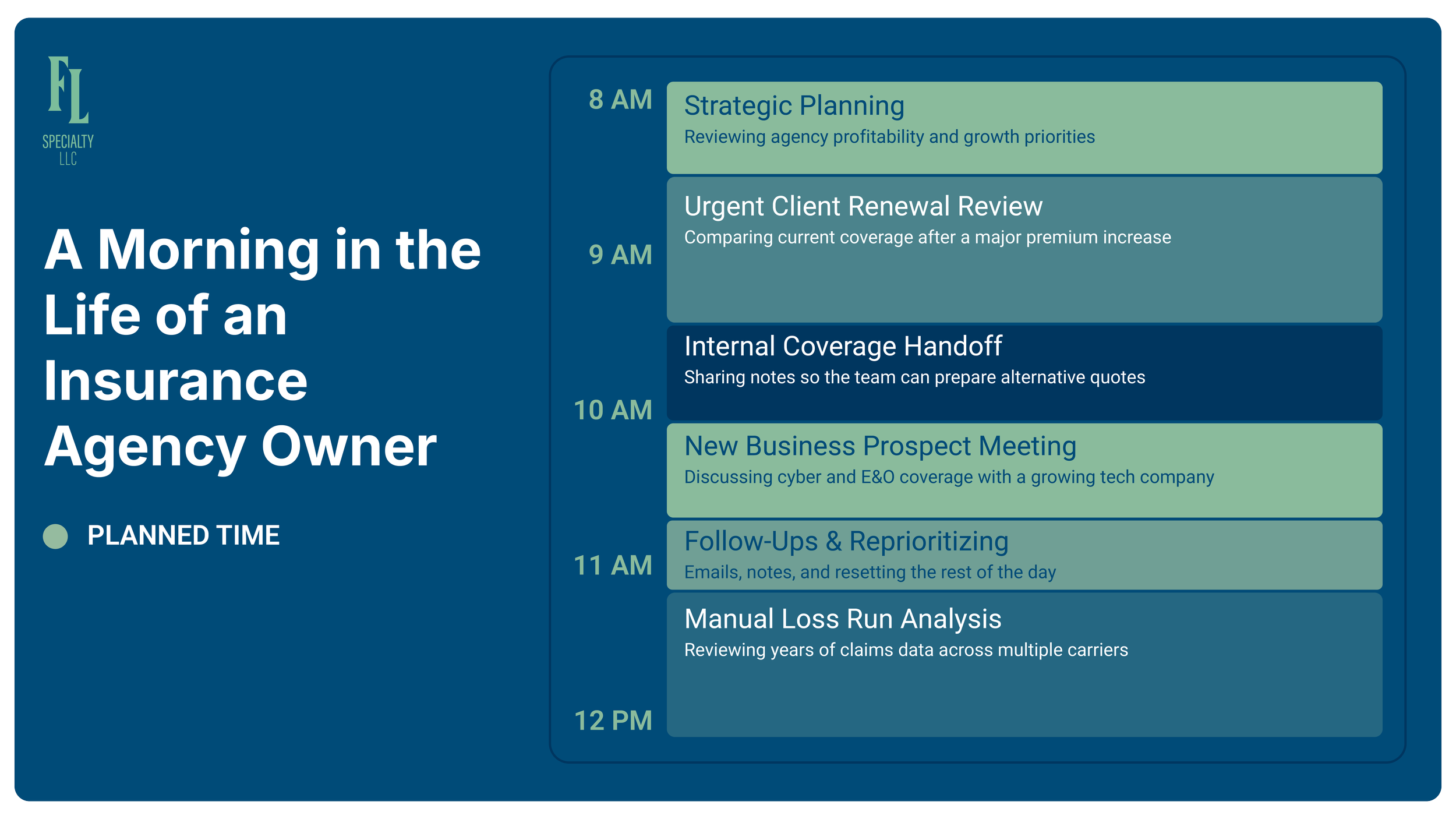

The Morning Scramble: When Strategy Meets Reality (8 AM - 12 PM)

Michael arrives at the office at 8 AM with coffee in hand and good intentions. He opens his laptop, pulls up the profitability analysis he started last week, and gets about seven minutes of focused work in before the first interruption.

His account manager knocks on the door.

A renewal just came in from their second-largest client—a manufacturer with a complex package policy. The incumbent carrier increased the premium by 18%, and the client is furious. They need quotes from at least three alternative carriers by Friday to have any chance of retaining the account. The account executive is out sick.

Can Michael help review the current coverage so they know what to quote?

What should take 15 minutes turns into an hour and a half.

Michael pulls up the current policy in the agency management system, opens multiple carrier portals, downloads PDFs, and starts building a spreadsheet to map coverages side by side. General liability is straightforward enough. The property schedule has 14 locations with varying limits. The umbrella has specific underlying requirements. There are three endorsements he needs to cross-reference.

His coffee goes cold.

By the time he hands off his notes, it’s 9:47 AM—and the strategic planning window is gone.

Moments later, a producer walks in with a prospect who wants to meet right now. They happened to be in the neighborhood. Michael shifts gears instantly.

The meeting actually goes well. The prospect is a growing tech company looking for a sophisticated cyber and E&O program. This is exactly the kind of business Michael wants more of—higher premium, better retention, clients who value expertise over price.

For a moment, he remembers why he became an insurance agency owner in the first place.

Then he checks his calendar.

He has 90 minutes before lunch and still needs to prepare a quote for a client with a brutal loss history.

Michael opens the loss runs—five years of claims data across three carriers, all formatted differently. He squints at PDFs, manually calculating frequency and severity trends. How many auto claims in the last three years? What’s the total incurred versus paid? Are the workers’ comp claims forming a pattern?

By noon, he has a headache, incomplete analysis, and zero progress on new business development.

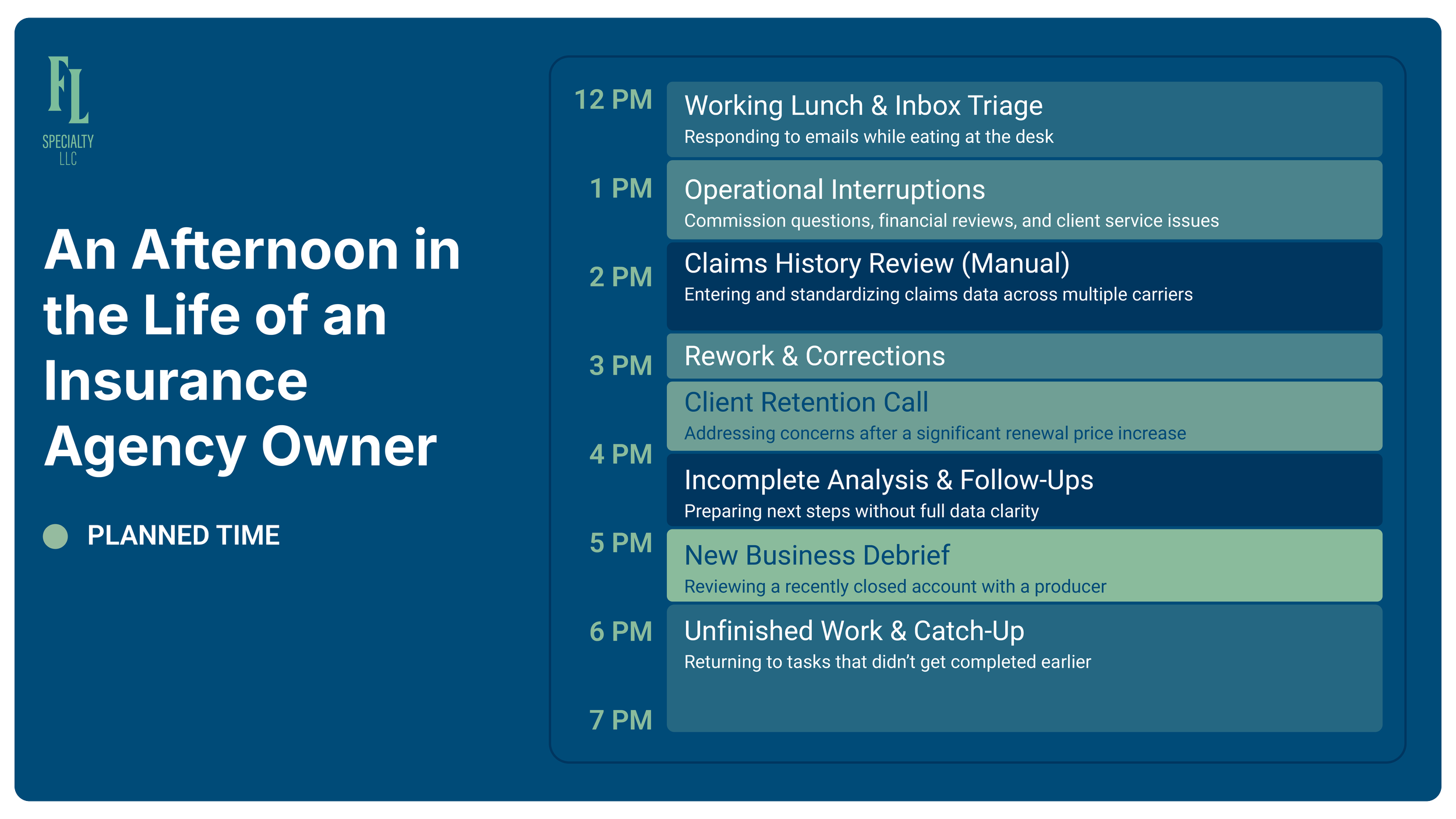

The Afternoon Push: Where Good Intentions Go to Die (12 PM - 5 PM)

Michael eats lunch at his desk while answering emails.

A producer asks about offering a lower commission split to win a large account. The bookkeeper needs financials reviewed before tomorrow’s bank meeting. A client calls—three times—because a certificate of insurance went to the wrong email address and is now holding up a job site.

At 1:30 PM, Michael gets back to the loss run analysis. He’s typing claim data into Excel, trying to normalize formats across carriers. One shows incurred amounts, another separates paid and reserved, a third lumps everything together.

An hour later, he realizes he misread the workers’ comp reserves and has to redo the calculations.

At 3 PM, the phone rings again.

It’s the client facing the 18% renewal increase. Another broker claims they can beat the price easily. Should they switch?

Michael tries to slow them down, explaining the importance of comparing coverage—not just price. But he doesn’t yet have the side-by-side analysis to back it up. He asks for 48 hours.

The client reluctantly agrees. The doubt is audible.

By 4:30 PM, a producer shares good news—they closed a solid account. But as they review the details, Michael realizes he doesn’t actually know their true win rate. How many quotes do they issue versus bind? Which carriers are they competitive with? Where are they losing deals—and why?

As an insurance agency owner, Michael is making strategic decisions based more on gut feel than data.

At 5:45 PM, most of the team left. Michael is still at his desk, circling back to unfinished work. He’ll likely be there until 7.

Where the Time Actually Goes for an Insurance Agency Owner

If Michael tracked his time honestly for a week, here's what he'd find:

35% – Operational firefighting: Jumping in to help with complex quotes, coverage questions, client escalations, and problems that "only the principal can handle."

25% – Client escalations: Taking calls from unhappy clients, smoothing over service issues, personally handling the biggest accounts when things go sideways.

20% – Team management: Answering questions, making decisions that should be delegated, mediating conflicts, covering for absent staff.

15% – Actual strategic planning: Profitability analysis, growth strategy, market positioning, carrier relationships, perpetuation planning—if he's lucky.

5% – Business development: The thing that's supposed to be his primary job as principal.

Here’s the uncomfortable truth: Michael was hired, or hired himself, to be the CEO of his agency.

Instead, he’s functioning as a very expensive account manager with an owner’s title.

The problem isn’t competence. The problem is that a massive portion of an insurance agency owner’s day is consumed by manual analytical work that technology should be handling.

The Technology Solution: Getting Your Time Back

For most insurance agency owners, the biggest bottleneck isn’t effort or expertise—it’s time. And more specifically, the amount of time consumed by manual analytical work that should no longer be manual.

This is where technology starts to fundamentally change the role of the insurance agency owner.

The Old Way: Coverage Comparison

Michael's account manager brings him a renewal. He:

Downloads current policy documents from 2-3 carrier portals (15 minutes)

Opens each PDF, searching for specific coverages and limits (30 minutes)

Builds an Excel spreadsheet to map everything side by side (45 minutes)

Cross-references endorsements and manually checks for gaps (30 minutes)

Formats it into something presentable for the client (20 minutes)

Total time: 2 hours and 20 minutes for a single policy comparison. If this is a complex account with multiple policies, add another hour. If the account executive needs to compare quotes from 3-4 markets, multiply accordingly.

The New Way: Quote & Policy Comparison Tool

Michael's account manager uploads the policy documents. The tool:

Automatically extracts all coverage details, limits, deductibles, and endorsements

Identifies the policy structure across all documents

Creates a side-by-side comparison highlighting differences

Flags potential gaps or coverage concerns

Generates a clean, client-ready report

Total time: 8 minutes.

Michael glances at the comparison on his screen, sees immediately that the competing quote has a lower product liability sublimit and a higher property deductible, and sends it to the account manager with notes. He's back to focusing on what he's actually good at—strategic client relationships—in the time it used to take him to find the right PDF.

The Old Way: Loss Run Analysis

That manufacturer with the tough loss history? Michael's process:

Opens loss run PDFs from multiple carriers (5 minutes)

Manually types claim data into Excel, fighting with different formats (90 minutes)

Calculates frequency, severity, and trends by hand (45 minutes)

Realizes he made an error, goes back to recalculate (30 minutes)

Tries to identify patterns that might concern underwriters (20 minutes)

Second-guesses whether his analysis is actually accurate (priceless anxiety)

Total time: 3+ hours of mind-numbing data entry and calculation. And he's still not confident he got it right.

The New Way: Loss Run Analyzer

Michael uploads the loss run documents. The tool:

Ingests loss data regardless of carrier format

Automatically normalizes and categorizes all claims

Calculates frequency and severity trends across time periods

Identifies patterns and outliers (e.g., "80% of claims occur in Q4")

Flags high-severity claims that will raise red flags for underwriters

Generates visual reports showing trends at a glance

Total time: 12 minutes from upload to insight.

Michael can now walk into an underwriter meeting or client conversation with confidence. He knows exactly what the loss history looks like, where the problems are, and what story the data tells. More importantly, he can spot these patterns before renewal time, giving him months to work with the client on loss control instead of scrambling at the last minute.

What Better Actually Looks Like

When insurance agency owners remove themselves from manual analysis, something important happens: they don’t just get time back, they get clarity.

Six months after implementing modern comparison and analysis tools, Michael’s day looks very different.

It's 7:15 AM on a Tuesday. His phone lights up with the same messages—a producer needs guidance, meetings are moving, clients have urgent questions. But when his account manager walks in at 8:30 with that renewal crisis, Michael doesn't disappear down a rabbit hole of manual analysis.

He opens the comparison tool, uploads the incumbent and competing policies, and has a clear coverage analysis in under 10 minutes. He spots immediately that the competing quote looks cheaper because it's missing $2M in umbrella coverage. He sends the account manager back with specific questions for the competitor and notes for the conversation with the client.

By 9 AM, he's already handled what used to take until lunch.

He still takes the walk-in meeting with the prospect—those relationship moments are what he's supposed to be doing. But when they discuss the cyber and E&O program, Michael can quickly pull up loss trends from similar clients in his book. He knows exactly where the agency is competitive and which carriers to approach first. The prospect is impressed by how prepared he is.

After lunch, Michael finally gets to that profitability analysis he's been putting off. With quote comparison data at his fingertips, he can see win rates by carrier and line of business. With loss run analysis streamlined, he can identify which clients are becoming risks before they blow up. He spends two uninterrupted hours on actual strategic planning.

At 3 PM, when the manufacturer client calls in a panic, Michael is ready. He's already run the loss analysis. He knows their frequency is trending down, their severity on the remaining claims is manageable, and they're actually a good risk that's been unfairly hammered by two large but unrelated losses. He talks the client off the ledge, articulates a data-driven story the new markets will understand, and sets up a meeting for tomorrow with a strategy in hand.

He leaves at 5:30. The work is done. The clients are taken care of. And he's spent his day doing what an agency principal should do—leading, strategizing, and growing the business.

That 35% he was spending on operational firefighting? Cut in half. That 5% on business development? Tripled. The profitability analysis that's been on his list for six months? Complete.

The Bottom Line for Principals

You didn’t build an agency to be the highest-paid data entry person in the building.

If you’re spending hours manually comparing policies and analyzing loss runs, that’s effectively what you’ve become. The agencies that thrive aren’t working harder—they’re removing the manual work that keeps owners stuck in operations instead of leadership.

The question isn’t whether you can keep doing things the old way.

It’s what it’s costing you in missed opportunities, stalled growth, and strategic work that never happens.

Want to see how agency principals are reclaiming their time? DM Quentin on LinkedIn to chat more.

Insurance Agency Owner FAQs

What does an insurance agency owner do day to day?

The day-to-day responsibilities of an insurance agency owner extend far beyond selling insurance. While priorities vary by agency size and structure, most owners spend their time overseeing renewals, managing carrier relationships, supporting producers and account managers, handling client escalations, and making strategic decisions about growth and profitability.

In reality, many insurance agency owners also find themselves deeply involved in operational work—reviewing complex policies, analyzing loss runs, and stepping in when the team is stretched thin. This operational pull often limits the time available for leadership and long-term planning.

What are the biggest challenges insurance agency owners face today?

One of the biggest challenges insurance agency owners face is time. Specifically, time lost to manual processes that pull owners into the weeds of day-to-day operations.

Common challenges include:

Managing complex renewals and coverage comparisons

Analyzing loss runs across multiple carriers and formats

Handling client escalations and retention pressure

Limited visibility into profitability, win rates, and carrier performance

Balancing growth initiatives with operational demands

These challenges aren’t a reflection of poor leadership—they’re often the result of outdated workflows and limited tooling.

Why do insurance agency owners spend so much time on operations?

Many insurance agencies still rely on manual, fragmented processes for tasks like policy comparison and loss run analysis. When those tasks become urgent—as they often do during renewal season—insurance agency owners are pulled in because the work is complex, high-stakes, and difficult to delegate.

Without better systems in place, owners become the default problem-solvers, spending hours on work that doesn’t require their level of experience or judgment.

How do insurance agency owners free up time for strategic planning?

Successful insurance agency owners free up time by reducing or eliminating manual analytical work. This often means adopting tools that automate time-consuming tasks like policy comparison and loss run analysis, standardizing workflows, and giving teams access to faster, more reliable insights.

When owners no longer have to build spreadsheets or manually normalize data, they can redirect their time toward leadership, growth strategy, and high-value client relationships.