AI Tools for Insurance: Why Carriers and Brokers Can’t Share the Same Technology

"Why can't brokers just use the same AI tools for insurance that carriers use?"

If you work in insurance technology, you've probably heard this question more times than you can count. On the surface, it seems like a reasonable question—after all, carriers and brokers operate in the same industry, work with the same products, and serve overlapping customer bases. So why shouldn't they use the same AI solutions?

The answer reveals a critical misunderstanding about how different segments of the insurance value chain actually operate. It's not just about having different preferences or priorities—carriers and brokers have fundamentally different business models that require completely different technological approaches.

Let me break down why one-size-fits-all AI fails in insurance, and what smart organizations are doing instead.

AI Tools for Insurance Carriers: Managing Risk at Scale

Insurance carriers operate as risk managers and financial institutions. Their entire business model revolves around accurately assessing risk, pricing policies appropriately, and managing large portfolios of policies to ensure profitability. As a result, AI tools for insurance carriers are built to optimize portfolios, pricing discipline, and long-term loss performance—not individual account relationships.

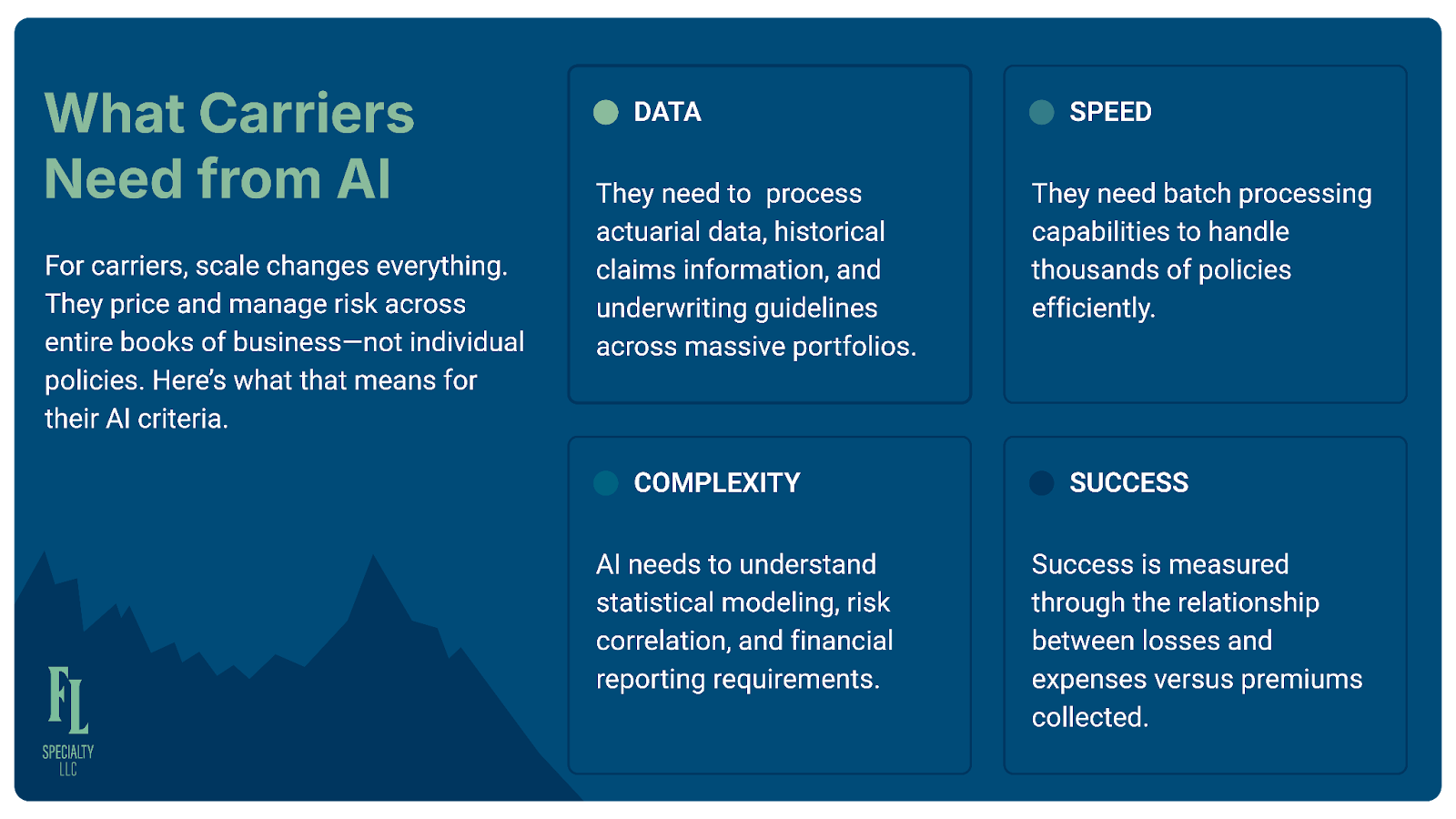

What carriers need from AI:

Carriers focus on portfolio risk management and pricing optimization. Every day, they're making decisions about thousands of policies simultaneously. Their AI needs to answer questions like: Is this book of business profitable? Are we pricing adequately for emerging risks? How should we adjust our appetite in specific segments?

The data carriers work with reflects this focus. They analyze loss ratios, claim patterns, renewal profitability, and loss development trends. Their systems process actuarial data, historical claims information, and underwriting guidelines across massive portfolios.

Speed matters differently for carriers. They need batch processing capabilities to handle thousands of policies efficiently. While individual policy decisions matter, carriers optimize for throughput and consistency across their entire book.

The complexity carriers face is deeply technical and mathematical. They're running actuarial models, calculating reserves, projecting loss development, and ensuring regulatory compliance. Their AI needs to understand statistical modeling, risk correlation, and financial reporting requirements.

Most importantly, carriers measure success through the combined ratio—the relationship between losses and expenses versus premiums collected. AI that doesn't directly impact this metric isn't delivering value in the carrier world.

AI Tools for Insurance Brokers and MGAs: Relationship-Driven Growth

Brokers and MGAs operate as advisors and intermediaries. Their business model depends on maintaining strong client relationships, understanding individual account needs, and optimizing placement across multiple carriers.

What brokers and MGAs need from AI:

Brokers focus on client relationship optimization and revenue growth. In practice, AI tools for insurance in the broker world surface insights about client behavior, renewal risk, and growth opportunities. They need to answer different questions: Which clients are at risk of leaving? Where are cross-sell opportunities? Which accounts deserve more attention? How can we improve our service delivery?

The data brokers work with is relationship-focused. They track account performance, renewal timing, client communication patterns, cross-sell opportunities, and competitive positioning. Their AI needs to understand client behavior, not just policy performance.

Speed means something different for brokers. They need real-time insights and opportunity alerts. When a client calls with a concern, brokers need immediate access to account intelligence. When renewal time approaches, they need proactive alerts and recommendations.

Broker complexity comes from managing relationships across multiple carriers. They're comparing quotes, optimizing placement strategies, coordinating submissions, and advocating for clients. Their AI needs to understand market dynamics, carrier appetites, and competitive positioning.

Brokers measure success through revenue per client and retention rates. AI that helps identify opportunities, improve service, or strengthen relationships delivers value in the broker world.

Why One-Size-Fits-All AI Tools for Insurance Don’t Work

Think about it this way: carriers think in terms of risk pools and loss development, underwriting profit and market share, rate adequacy and regulatory compliance.

Brokers think in terms of client satisfaction and retention, commission optimization and growth, competitive positioning and service differentiation.

It's analogous to asking whether a manufacturer can use the same tools as a retailer. Both work with products. Both need inventory management and customer service. But their core business models, success metrics, and daily operations are completely different. The manufacturer optimizes production efficiency and cost control. The retailer optimizes merchandising, customer experience, and sales velocity.

Similarly, while carriers and brokers both work in insurance, they're essentially playing different games. Carrier AI built for portfolio risk management will frustrate brokers who need client intelligence. Broker AI designed for relationship optimization won't address the actuarial and regulatory requirements carriers face.

What Smart Organizations Are Doing

Forward-thinking insurance organizations recognize these differences and tailor their AI strategies accordingly. Instead of adopting generic AI tools for insurance, they align technology investments to their role in the value chain.

Carriers are deploying AI for underwriting automation, pricing optimization, and portfolio management. They're using machine learning to improve risk selection, predictive modeling to anticipate losses, and natural language processing to extract insights from claims data.

Brokers are implementing AI for client intelligence, opportunity identification, and renewal optimization. They're using AI to analyze communication patterns, predict client needs, identify cross-sell opportunities, and prioritize accounts for attention.

MGAs occupy an interesting middle ground, combining elements of both approaches. They need portfolio management capabilities like carriers, but they also need client advisory tools like brokers. The most successful MGAs are building hybrid AI strategies that address both sides of their business model.

Finding Your AI Strategy

The key question isn't "What AI tools for insurance should companies use?" but rather "What business model are you supporting?"

Are you a carrier looking to optimize underwriting accuracy and portfolio profitability? Your AI strategy should focus on risk assessment, pricing optimization, and claims prediction.

Are you a broker or MGA focused on client growth and retention? Your AI strategy should emphasize relationship intelligence, opportunity identification, and service delivery optimization.

The insurance industry doesn't need more generic AI solutions. It needs purpose-built tools that understand the unique challenges, data structures, and success metrics of each part of the value chain.

The organizations that will win in the AI-powered insurance future aren't the ones with the most technology—they're the ones with the right technology for their specific business model.

Where does your organization sit—carrier, broker, or MGA—and how are you thinking about AI this year? The answers often reveal more about business strategy than technology itself. If you’re evaluating how AI fits into your model, contact us to continue the conversation.