Behind the Desk: A Day in the Life of an Insurance Account Manager

It's 8:03 AM on a Thursday, and Rachel's inbox already has 47 unread emails. She opens her renewal tracking spreadsheet—18 accounts are up for renewal this month, and 6 of them renew in the next 10 days. Her producer just forwarded her a renewal comparison request that needs to be done by end of day. A client emailed at 6:47 AM asking why their renewal premium jumped 38%.

Before she can even prioritize, her phone rings. Another client needs a certificate of insurance in 15 minutes. She handles it quickly and gets back to the real problem: she's got hours of policy comparison and loss run analysis ahead of her, and none of it can wait.

If you're an insurance account manager, you already know how this day is going to go. You're the glue holding everything together—the person who keeps clients from walking out the door when renewals go sideways. But you're doing it by manually building spreadsheet comparisons and decoding carrier loss run formats, with everyone expecting you to have instant answers to questions that require hours of document analysis.

And while job descriptions for an insurance account manager talk about proactive service, strong client relationships, and strategic account oversight, the reality inside most agencies looks very different.

To understand why, it helps to look at what the role of an insurance account manager is supposed to be—and then compare it to how the day actually unfolds.

What Is an Insurance Account Manager?

An insurance account manager is responsible for servicing and managing client accounts inside an insurance agency or brokerage. While producers focus on bringing in new business, insurance account managers ensure existing clients receive consistent service, policy support, and renewal management.

Typical insurance account manager responsibilities include:

Managing certificates of insurance and endorsement requests

Preparing renewal comparisons and assisting producers during renewal season

Reviewing policies and endorsements to answer coverage questions

Analyzing loss runs and claims history

Communicating with carriers about coverage details and underwriting requirements

Maintaining client records in the agency management system (AMS)

Helping identify coverage gaps and supporting retention efforts

In theory, the role is designed to be proactive—helping clients understand their coverage, preparing accounts well before renewal, and strengthening long-term relationships.

But in many agencies, the reality is that insurance account managers spend the majority of their day reacting to urgent requests, digging through policy documents, and manually compiling information.

Which brings us back to Rachel's Thursday morning.

The Morning Scramble: A Typical Morning for an Insurance Account Manager (8 AM - 12 PM)

At 8:30 AM, her producer walks over. "Hey, that renewal for Johnson Manufacturing—can you pull together a comparison of the incumbent and the two quotes I got? Client wants to see it before their board meeting tomorrow morning."

Rachel's heart sinks. Johnson Manufacturing is complex—package policy with property, GL, auto, umbrella, and cyber. The incumbent is with one carrier. The two competing quotes are from different carriers with completely different structures.

She knows what this means: 3-4 hours building a spreadsheet, hunting through policy documents, extracting limits and deductibles, trying to create an apples-to-apples comparison.

"When do you need it?"

"End of day would be great. Client's meeting is at 9 AM tomorrow."

Of course it is.

By 11:30 AM, Rachel has made it through General Liability and Property coverage in the Johnson comparison. She's got Auto, Umbrella, and Cyber still to go. She's already found two potential coverage gaps in Quote #1 that she needs to flag—but she's not entirely certain she's reading the endorsements correctly.

Her phone rings. Another client needs an endorsement for a new location opening next week. They forgot to mention it until now.

She puts the Johnson comparison aside—again—and shifts gears. By noon, she's handled three more certificate requests, answered two coverage questions she wasn't completely sure about, and made zero progress on the comparison.

The Afternoon Push: Renewal Chaos and Information Black Holes (12 PM - 6 PM)

At 1:00 PM, Rachel pulls up her renewal tracking spreadsheet. Six accounts renew next week. One of them—a $31K revenue contractor account—just had their renewal quote come in this morning. 38% increase. The client is going to lose their mind.

Rachel needs to understand why before the client calls screaming. She downloads the renewal quote and the loss runs from the carrier portal. The loss runs are five years of claims data—14 pages in a format designed to be unreadable. Dates, claim numbers, amounts paid, amounts incurred, reserves, status codes.

Rachel starts building a spreadsheet. Claim date, type, incurred, paid, status. She's manually typing from the PDF. "03/15/2021, AUTO, $15,847 incurred, $12,200 paid, Closed." Next claim. And the next.

Forty minutes later, she's only made it through two of the five years. Her eyes are glazing over.

At 2:15 PM, her phone rings. It's the contractor client. They just got the renewal quote. They're furious about the 38% increase. What's going on?

Rachel hasn't finished the loss analysis. She doesn't have good answers yet. She tells the client she's working on it and will get back to them by end of day. The client is not happy. "I've been with you guys for seven years, and this is how you treat me? Maybe I should talk to other brokers."

Rachel goes back to manually entering claim data. This is going to take at least another hour and a half, and she's still not confident she'll interpret the patterns correctly.

At 3:00 PM, her producer stops by. "How's that Johnson Manufacturing comparison coming?"

Rachel looks at her screen—still only halfway done. "Should have it by end of day."

She's now committed to finishing two major projects before 5 PM, plus handling whatever other fires pop up. She knows she's going to be here until 7 PM. Again.

At 4:45 PM, Rachel frantically finishes the Johnson comparison. The Cyber coverage is giving her fits—all three policies have completely different structures. She's doing her best but isn't sure she's capturing all the nuances.

She sends it to the producer at 5:12 PM with a note: "A few areas I wasn't 100% certain on—highlighted in yellow."

At 5:20 PM, she's still working on the loss run analysis for the contractor. She's finally got all the claims entered. Now she needs to calculate frequency, severity trends, identify patterns.

At 5:47 PM, she thinks she's got it. Eight claims in the past 3 years—frequency is concerning. Two large GL claims pushed the total incurred way up. She writes an email to the client explaining what's driving the increase, knowing she doesn't have alternative quotes yet—that's going to take another day or two.

She leaves at 6:45 PM, exhausted.

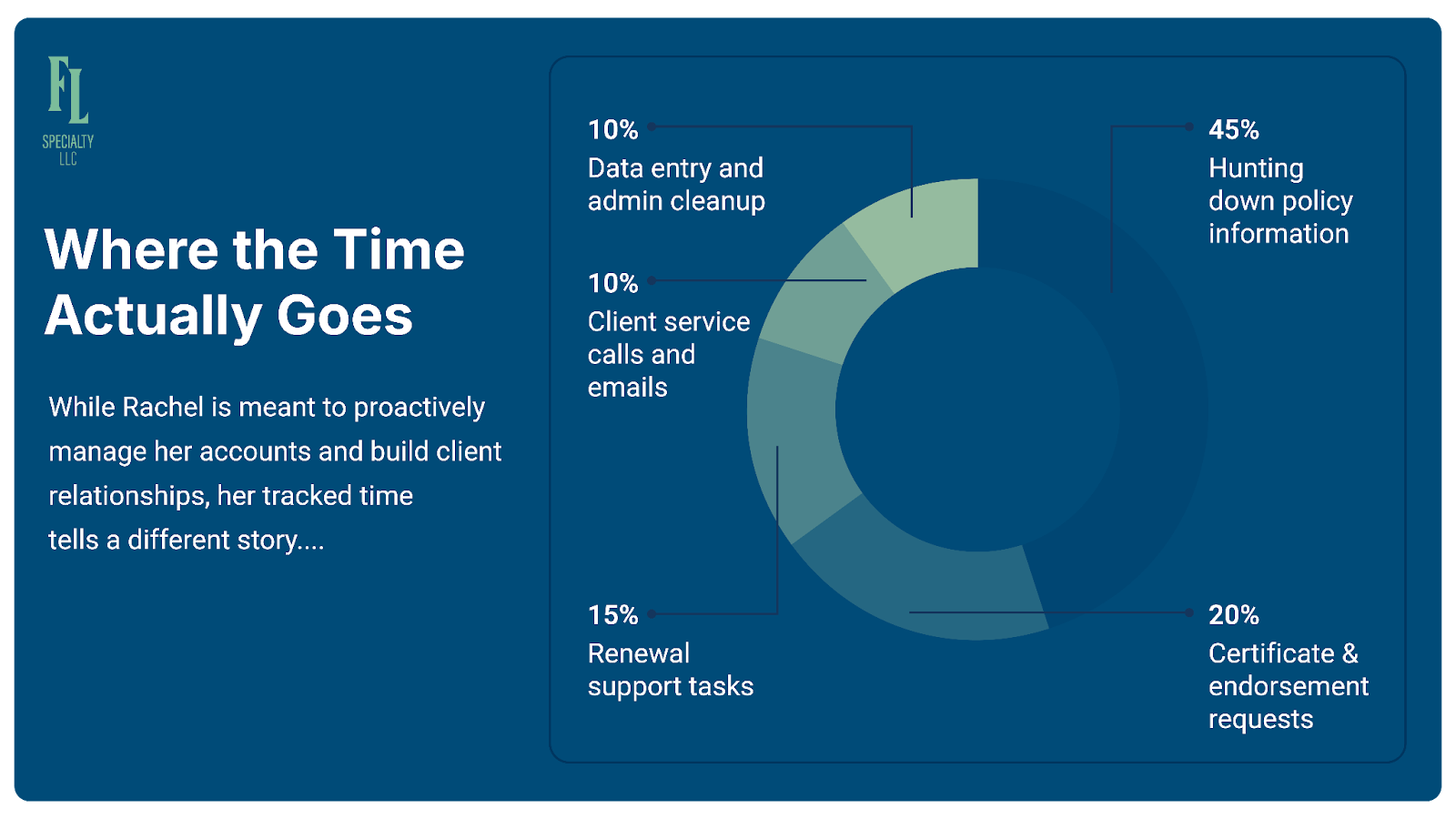

Where the Time Actually Goes for an Insurance Account Manager

Rachel is supposed to be an insurance account manager. Her job description mentions "proactive account management," "building client relationships," and "ensuring superior service delivery."

But if she tracked her time honestly:

45% – Hunting down policy information: Logging into carrier portals, downloading documents, searching through PDFs, extracting coverage details.

20% – Certificate and endorsement requests: Processing certs, chasing information, reissuing documents.

15% – Renewal support tasks: Building comparisons, analyzing loss runs, gathering information—usually in last-minute panic mode.

10% – Client service calls and emails: Answering questions, explaining coverages, managing expectations.

10% – Data entry and administrative cleanup: Updating the AMS, filing documents, maintaining records.

0% – Proactive account management: Reviewing accounts before renewal, identifying coverage gaps, reaching out to clients with recommendations—the thing she's supposed to be doing.

That last number—zero—is the real problem. Rachel spends her entire day reacting to urgent requests and hunting for information. She has no time for the proactive work that would actually prevent half the fires she's putting out.

The Technology Solution: Getting Ahead of the Chaos

The Old Way: Answering Coverage Questions

Client calls: "Does my policy cover damage to customer property in our care?"

Rachel's process:

Search for client in AMS (2 minutes)

Download current policy from carrier portal (3 minutes including login issues)

Open 62-page PDF

Search for "care, custody, control" (5 minutes)

Find exclusion language on page 18, endorsement on page 34, definitions on page 7

Try to understand how they all interact (15 minutes)

Call carrier to confirm understanding (10 minutes if they answer)

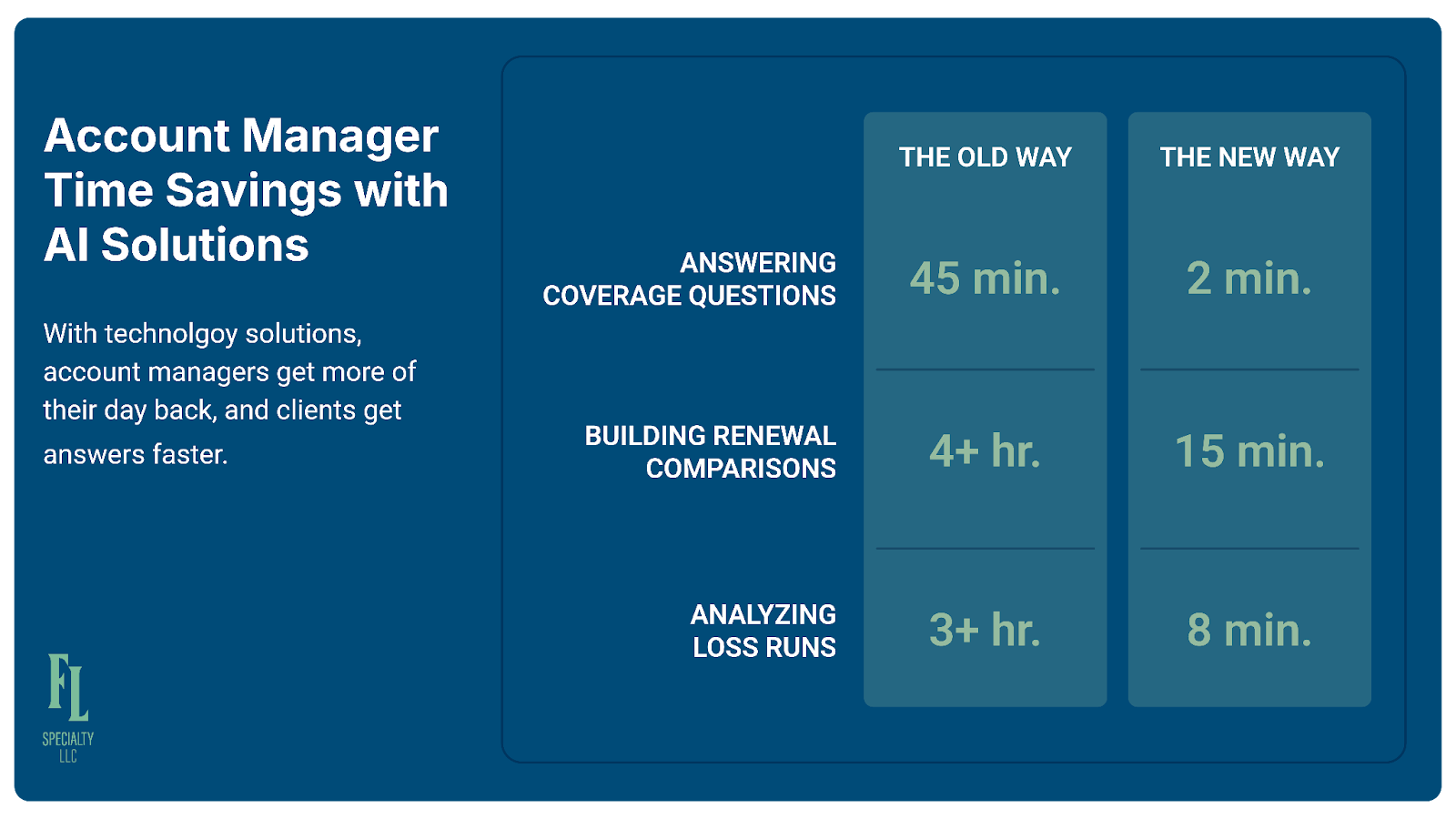

Total time: 30-45 minutes for what should be a simple question. With five of these per day, that's 2-3 hours just hunting through documents.

The New Way: Quote & Policy Comparison Tool

Rachel opens the comparison tool, searches for the client, and the tool shows: "Care, Custody, and Control Exclusion applies - No coverage for property in insured's care. Bailee coverage not included."

Total time: 2 minutes with confidence in the answer.

Rachel can now answer coverage questions in real-time while the client is on the phone, looking knowledgeable instead of saying "let me research that and get back to you."

The Old Way: Building Renewal Comparisons

Johnson Manufacturing renewal—incumbent plus two competing quotes:

Download all documents (5 minutes)

Build Excel comparison structure (10 minutes)

Search through incumbent for GL limits—found on page 12, modified by endorsement on page 34 (15 minutes)

Search through Quote 1 (20 minutes—different structure)

Search through Quote 2 (18 minutes—package format)

Repeat for Property (45 minutes), Auto (40 minutes), Umbrella (35 minutes), Cyber (50 minutes)

Identify coverage gaps (30 minutes)

Format (20 minutes)

Total time: 4+ hours. With three major renewals the same week, she's spending 12+ hours just building comparisons.

The New Way: Quote & Policy Comparison Tool

Rachel uploads the incumbent and two competing quotes. The tool:

Extracts all coverage limits, deductibles, endorsements

Creates side-by-side comparison across all coverages

Highlights key differences and flags coverage gaps

Generates clean comparison report

Total time: 15 minutes including review.

Rachel just reclaimed 3+ hours. She can handle multiple renewals without staying until 8 PM and can actually get ahead of renewals instead of constantly scrambling.

The Old Way: Analyzing Loss Runs

Contractor renewal is 38% higher. Rachel needs to understand why:

Download loss runs (5 minutes)

Create Excel spreadsheet (5 minutes)

Manually type 5 years of claim data (90 minutes)

Fix errors (15 minutes)

Categorize by type (20 minutes)

Calculate frequency and severity (30 minutes)

Identify patterns (30 minutes)

Build summary (20 minutes)

Total time: 3+ hours of data entry and she's still not confident she's reading it correctly.

The New Way: Loss Run Analyzer

Rachel uploads the loss run PDF. The tool:

Extracts all claim data regardless of format

Categorizes by type, calculates trends

Identifies patterns: "8 claims in past 3 years vs. 2 in prior 3 years. Two large GL claims totaling $87K significantly elevated total incurred."

Generates charts and summary

Total time: 8 minutes.

When the client calls upset, Rachel already has answers: "Your frequency increased significantly—8 claims in 3 years compared to only 2 before. Plus two large GL claims totaling $87K. The carrier is seeing both frequency and severity concerns."

She sounds knowledgeable and proactive instead of caught off guard.

What Better Actually Looks Like for an Insurance Account Manager

Six months later, Rachel's days are still busy, but the chaos has been replaced with control.

At 8:03 AM, when that cert request comes in, Rachel uses the comparison tool to confirm coverage details in seconds and issues the cert in under 5 minutes.

At 8:30 AM, the coverage question arrives. Rachel searches the client's policies, finds the answer immediately, and responds with a clear answer while suggesting they consider adding bailee coverage at renewal. The client is impressed.

When her producer asks about Johnson Manufacturing at 9:15, Rachel uploads the policies, runs the comparison, adds her notes, and sends it back in 20 minutes. The producer is amazed. "This used to take you half a day."

That $31K contractor account? Rachel uploaded the loss runs to the analyzer two weeks ago. She already knows what's driving the increase and has briefed the producer, who's already marketing to other carriers.

When the client calls at 2:15 PM upset about the increase, Rachel's prepared. She explains exactly what the carrier saw, shows them the data, and tells them about the alternative quotes already in progress. The client says, "I appreciate you staying on top of this."

At 3:00 PM, Rachel does something she hasn't done in months: she proactively reviews accounts renewing in 60 days, flags two that need attention, and sends notes to the producers about potential issues before renewal crunch time hits.

This is the proactive account management Rachel was hired to do—but never had time for.

At 5:30 PM, Rachel leaves on time. Her renewals are on track. She's responded to every client question. And she's made progress on proactive work instead of just reacting to fires.

Next month's retention numbers tell the story: 94% retention rate, up from 87%. Client satisfaction scores are up. And Rachel isn't burned out anymore.

The Bottom Line for an Insurance Account Manager

You're supposed to be managing accounts and building relationships, not spending 45% of your day hunting through carrier portals and typing data from PDFs.

Every hour you spend on manual extraction is an hour you're not doing proactive account management. Every time you tell a client "let me research that" when you should have the answer immediately, you're eroding their confidence.

If 60% of your time goes to hunting for information and building comparisons manually, you're only operating at 40% capacity as an actual insurance account manager.

The agencies where account managers are thriving—where retention is high and burnout is low—aren't working harder. They're eliminating the manual grunt work that turns account management into an impossible job.

Rachel still manages a full book of accounts. But now she spends her time answering questions immediately, getting ahead of renewals, identifying opportunities, building relationships. The manual work that used to dominate her day now happens in minutes.

Her clients get faster responses, better service, proactive recommendations. They feel taken care of instead of tolerated.

And Rachel finally feels like she's doing the job she was hired to do.

Ready to spend your days managing accounts instead of hunting for information? DM Quentin on LinkedIn to chat more.

FAQs About the Insurance Account Manager Role

What does an insurance account manager do?

An insurance account manager supports producers by servicing client accounts. Their responsibilities include preparing renewal comparisons, issuing certificates of insurance, processing endorsements, reviewing policies, answering coverage questions, and coordinating with carriers to resolve issues.

What is the difference between an insurance producer and an insurance account manager?

An insurance producer is responsible for sales and bringing in new business, while an insurance account manager focuses on servicing existing clients. Producers generate revenue through new accounts, while account managers help retain and grow those accounts through strong service and renewal management.

Do insurance account managers need a license?

In most states, insurance account managers must hold a property and casualty insurance license if they discuss coverage, advise clients, or process policy changes.

Is insurance account manager a stressful job?

The role can be demanding because insurance account managers handle multiple renewals, client requests, and urgent coverage questions simultaneously. Agencies that rely heavily on manual processes often create the most stress, while agencies with strong systems and automation allow account managers to focus on proactive service.