Behind the Desk: A Day in the Life of an Insurance CSR

It's 8:47 AM on a Tuesday, and Lisa's phone has already rung 12 times. She's got four certificate requests in her queue, three voicemails from clients asking coverage questions, and an email from a frustrated policyholder who wants to know why their deductible is different than they thought it was.

Lisa works as an insurance CSR (customer service representative), the frontline professional responsible for helping clients understand their policies, processing requests, and keeping accounts running smoothly.

If you work inside an insurance agency, you know the insurance CSR role is one of the most important and most demanding positions in the office.

But what does an insurance CSR actually do day to day? And why do so many insurance customer service representatives feel overwhelmed by information requests, policy questions, and certificate processing?

In this article, we’ll walk through a realistic day in the life of an insurance CSR, explore the most common responsibilities of the role, and look at how better systems can transform the way CSRs serve clients.

What Is an Insurance CSR?

An insurance CSR (customer service representative) is responsible for managing client service inside an insurance agency. Insurance CSRs work closely with producers, account managers, and carriers to help policyholders understand their coverage and keep their policies up to date.

In many agencies, the insurance CSR is the primary point of contact for clients, meaning they play a critical role in the client experience and overall agency reputation.

While producers focus on sales and bringing in new business, insurance CSRs focus on servicing existing clients—answering questions, processing documentation, and ensuring policies remain accurate and compliant.

The role requires a unique mix of technical insurance knowledge, organization, and customer service skills, because clients expect fast answers to questions that often require digging through policy documents, carrier portals, and agency systems.

And that’s where the real challenge begins.

To understand what the insurance CSR role actually looks like in practice, let’s walk through a typical morning inside an insurance agency.

The Morning Rush: When Every Question Requires a Scavenger Hunt (8 AM - 12 PM)

Lisa pulls up the client in the AMS while they're still on the phone. She sees they have a general liability policy with Carrier A. The deductible field in the AMS is blank. She needs to check the actual policy.

She puts the client on hold, logs into Carrier A's portal—the login is slow this morning—navigates to the client's policy, and downloads the declarations page. She opens the PDF and searches for "deductible." There it is: $2,500 per occurrence.

"Okay, I've got it—your property deductible is $2,500 per occurrence," Lisa says.

Total time: 4 minutes for what the client thought would be a 10-second answer.

As soon as she hangs up, another call comes in. "Hi Lisa, I need a certificate of insurance for a job site. Can you send it to me right away?"

Lisa takes down the certificate holder information and starts the process. She needs to verify the current policy details—effective dates, limits, coverage types. The client has GL with Carrier A, Auto with Carrier B, Workers Comp with Carrier C.

She starts filling out the ACORD certificate form, pulling information from three different places. The Auto policy—she needs to check the carrier portal because the umbrella endorsement isn't showing up correctly in the system. She downloads the auto policy, searches for the hired and non-owned auto coverage.

Fifteen minutes later, she's got the certificate ready and emails it over. One down, three more in the queue.

At 9:15 AM, her phone rings again. "Lisa, we just got our renewal and I don't understand why our premium went up so much. Can you explain what happened?"

Lisa pulls up the account. She can see the renewal quote showing an 18% increase. But she doesn't know WHY. She doesn't have the loss runs in front of her. She doesn't know if this client had claims that drove the increase.

"Let me pull your information and have someone call you back with a detailed explanation," Lisa says.

The client is annoyed. "I just want to know if we had claims. Do we have claims?"

Lisa doesn't have that information readily available. She'd need to log into carrier portals, download loss runs, review them—work that would take 30+ minutes.

"Let me get that information pulled together and either I or your account manager will call you back within the hour," Lisa promises.

At 10:00 AM, another call: "What's covered under our cyber policy? We had a potential incident and need to know if we should file a claim."

Lisa downloads the 45-page cyber policy and starts searching for coverage triggers. The client is waiting on the phone. Lisa is scrolling through the PDF trying to find the relevant section.

She's not 100% confident she's interpreting the coverage correctly. "Let me have your account executive review this specific situation and call you back to make sure we're giving you accurate guidance," she finally says.

Another "let me get back to you." The client sounds frustrated.

By 11:30 AM, Lisa has handled 18 calls, processed 3 certificates, and created 5 follow-up tasks for account managers and producers because she didn't have the information needed to answer questions on the spot. She feels like she's not actually helping anyone—just playing telephone between clients and people who have access to better information.

The Afternoon: Drowning in Information Requests (12 PM - 5 PM)

At 1:15 PM, a client emails: "Can you send me a copy of our current auto policy? Need it for an audit."

Lisa logs into Carrier B's portal, locates the policy, downloads it, and emails it to the client. Another 10 minutes.

At 2:00 PM, her phone rings. "Lisa, I'm looking at my bill and the premium is different than what I expected. Can you explain the breakdown?"

Lisa downloads the actual billing statement from the carrier to see what the client is seeing. Fifteen minutes later, she's walked the client through their bill—time that should have taken 2 minutes if the information was readily accessible.

At 3:00 PM, renewal season is hitting hard. Lisa's phone is ringing with clients who received their renewal quotes and have questions. "Why did my rate go up?" "Did we have claims?" "What's different about this quote versus last year?"

Lisa doesn't have easy access to loss histories or policy comparison information. She's taking messages and creating follow-up tasks for the account managers and producers who can actually answer these questions. But clients are frustrated that they can't get immediate answers from the first person they talk to.

At 4:00 PM, Lisa gets an urgent call. "I need a certificate RIGHT NOW for a job starting in 30 minutes."

Lisa drops everything, pulls up the client, starts filling out the certificate, realizes she needs to verify umbrella coverage limits, logs into the carrier portal—the portal is running slow—waits for the PDF to load, finds the information, completes the certificate, and emails it.

Twenty minutes. The client is stressed but grateful. Lisa is exhausted.

At 5:00 PM, Lisa looks at her task list. She completed 14 certificate requests today. She answered 47 phone calls. She created 12 follow-up tasks for other team members. She spent approximately 6 hours just searching for information across multiple systems and carrier portals.

And she feels like she barely helped anyone.

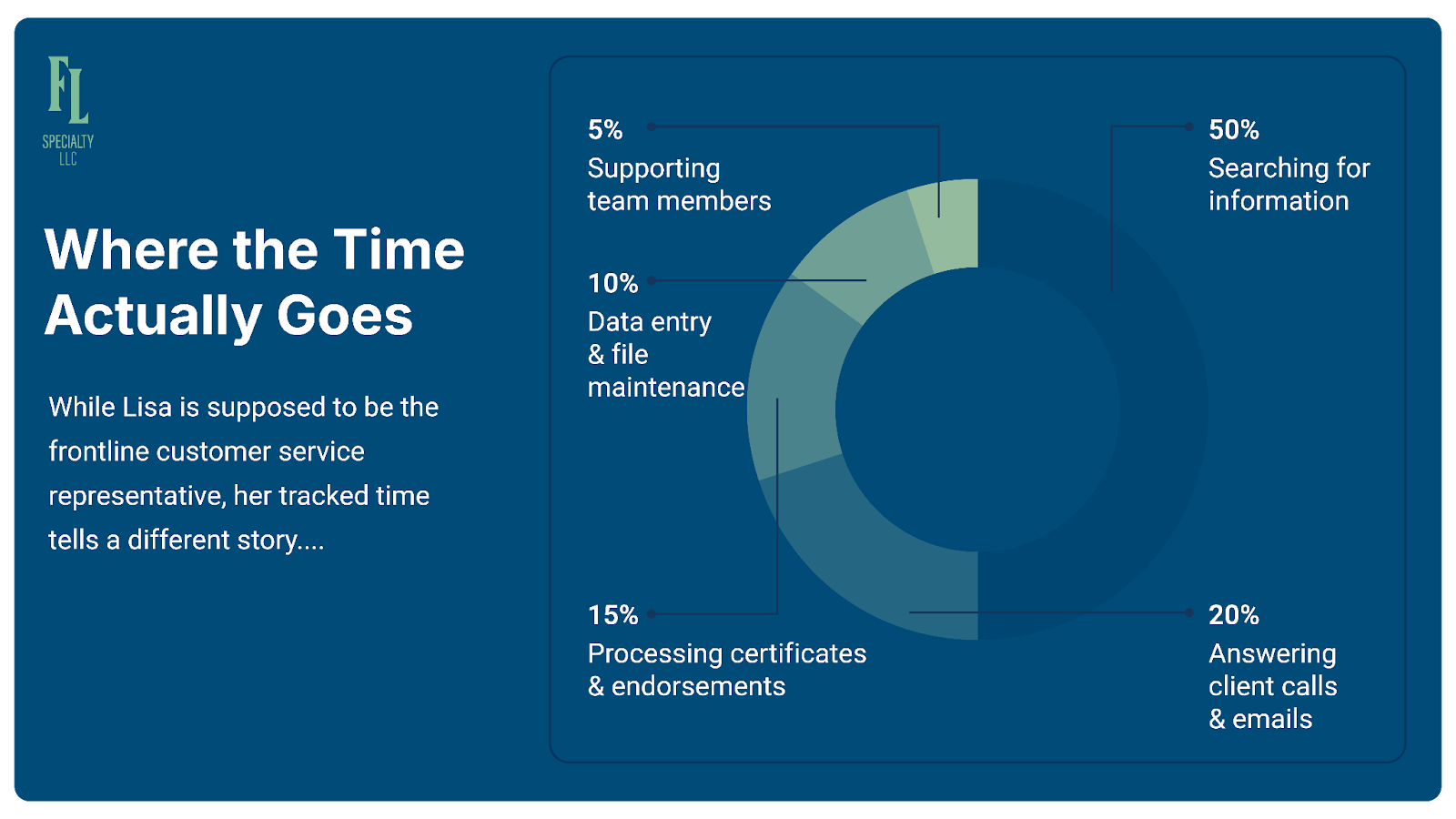

Where the Time Actually Goes

Lisa is supposed to be the frontline customer service representative—the friendly, knowledgeable first point of contact who makes clients feel taken care of.

But if she tracked her time honestly:

50% – Searching for information: Logging into carrier portals, downloading policy documents, hunting through PDFs, trying to find coverage details that should be instantly accessible.

20% – Answering client calls and emails: The actual customer service part—but often she's just taking messages because she doesn't have the information clients need.

15% – Processing certificates and endorsements: Each requiring hunting down policy information from multiple sources.

10% – Data entry and file maintenance: Updating systems, filing documents, keeping records current.

5% – Supporting other team members: Pulling information for account managers and producers who need policy details.

Lisa spends half her day just trying to FIND information, not actually serving customers. Every simple question becomes a 10-15 minute information retrieval project. And clients notice. They get frustrated. They start wondering if their agency really has their act together.

The Technology Solution: Becoming the Customer Service Superstar

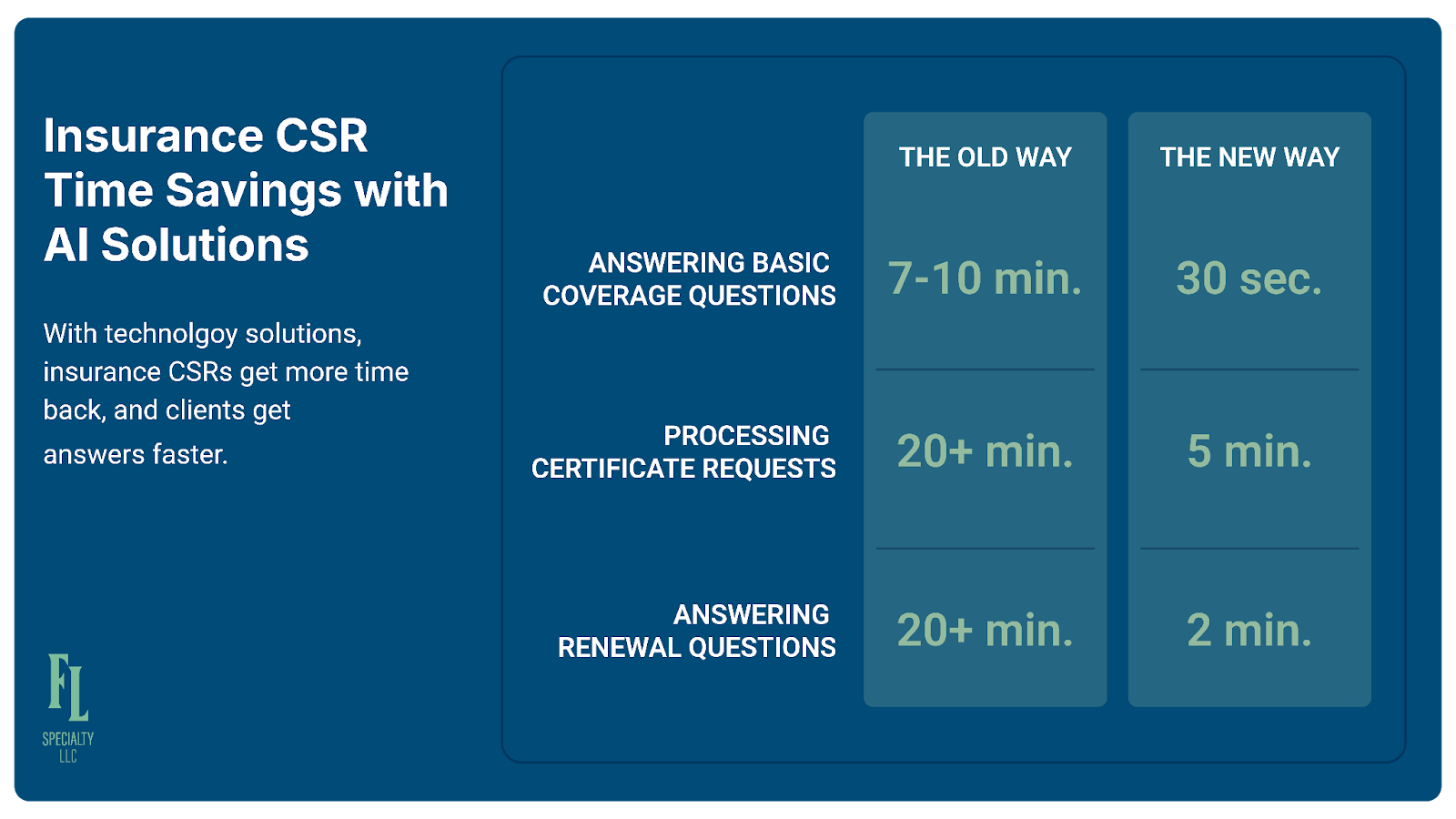

The Old Way: Answering Basic Coverage Questions

Client calls: "What's my general liability deductible?"

Lisa's process:

Pull up client in AMS (1 minute)

See that deductible field is blank in system

Log into carrier portal (1 minute)

Navigate to client's policy (2 minutes)

Download declarations page PDF (1 minute)

Open PDF and search for deductible (2 minutes)

Total time: 7-10 minutes for what should be a 30-second answer. Multiply by 15-20 similar questions per day, and Lisa is spending 2+ hours just looking up basic policy information.

The New Way: Quote & Policy Comparison Tool

Lisa opens the comparison tool, searches for the client, and sees all current policy details instantly displayed: GL deductible $2,500, limits $2M/$4M, effective dates, all endorsements. She answers immediately while the client is still on the phone.

Total time: 30 seconds.

Lisa now sounds knowledgeable and responsive instead of saying "let me look that up and call you back." The client feels taken care of.

The Old Way: Processing Certificate Requests

Client needs certificate showing GL, Auto, and Workers Comp:

Pull up client in AMS (1 minute)

Log into Carrier A portal for GL details (2 minutes)

Download GL policy to verify limits (2 minutes)

Log into Carrier B portal for Auto (2 minutes)

Download Auto policy to check hired/non-owned (3 minutes)

Log into Carrier C portal for Workers Comp (2 minutes)

Fill out ACORD form from three different sources (8 minutes)

Total time: 20+ minutes per certificate. With 10-15 requests per day, Lisa is spending 3-4 hours just gathering information to fill out forms.

The New Way: Quote & Policy Comparison Tool

Lisa opens the comparison tool—all current policy details instantly displayed: GL limits, Auto coverage including hired/non-owned, Workers Comp coverage. She fills out the ACORD form with all information in one place and sends.

Total time: 5 minutes.

Lisa just reclaimed 15 minutes per certificate request. That's 2-3 hours per day available for actual customer service.

The Old Way: Answering Renewal Questions

Client calls upset about renewal increase: "Why did my premium go up? Did we have claims?"

Lisa can see the increase in the system but doesn't have loss run information readily available. She'd need to log into the carrier portal, download loss runs, and review them—20+ minutes of work she doesn't have time to do, resulting in "Let me have your account manager call you back" and a frustrated client who has to wait.

The New Way: Loss Run Analyzer

Lisa opens the loss analyzer and sees the summary instantly: "3 claims in past 3 years totaling $47K. Frequency increase from prior period. One large property claim $28K in 2024."

She can give the client immediate context: "You had three claims in the past three years with total losses of $47K. The carrier is primarily concerned about the frequency increase and one large property claim from last year. Your account manager has been working on this and has alternative quotes in progress. They'll call you this afternoon with options."

Total time: 2 minutes and the client gets an informed answer instead of "let me get back to you."

What Better Actually Looks Like

Six months later, Lisa's days are still busy, but the constant frustration has been replaced with actual satisfaction.

When that client calls asking for their GL deductible, Lisa opens the comparison tool, sees the information instantly, and answers while the client is still on the phone. "Your GL deductible is $2,500 per occurrence. Anything else I can help you with?"

The client is pleasantly surprised. "Wow, that was fast. Thanks!"

The renewal question call comes in, but now Lisa has the loss analyzer open. She can see the client had 3 claims totaling $47K, which explains the 18% increase. She explains it clearly, mentions that their account manager is already working on alternative quotes, and the client hangs up feeling informed instead of frustrated.

By 11:30 AM, Lisa has handled 18 calls and actually HELPED people instead of just taking messages. She's processed 5 certificates in the time it used to take to do 2. And she hasn't said "let me get back to you" once for basic information.

At 5:00 PM, Lisa looks at her day. She completed 22 certificate requests—8 more than her old average. She answered 52 phone calls and actually resolved most of them on the first contact. She spent maybe 2 hours searching for information instead of 6.

Most importantly: she feels like she actually helped people today. Clients said "thank you" and meant it. Nobody was frustrated by long wait times for basic answers. Lisa went home feeling competent instead of exhausted.

Her manager notices too. Client satisfaction scores for first-contact resolution are up 40%. The number of callbacks is down dramatically. And Lisa—who was seriously considering leaving for a less stressful job—is actually enjoying her work again.

The Bottom Line for Insurance CSRs

You're the first person clients talk to. You set the tone for the entire relationship. When you sound knowledgeable and responsive, clients feel confident in their agency. When you're constantly saying "let me look that up and get back to you," clients start wondering if they should find a broker who has their act together.

But it's not your fault. You're not slow or incompetent. You're handicapped by systems that make simple questions take forever to answer.

If you're spending 50% of your day just searching for information, you're only operating at half capacity as an actual customer service representative.

The agencies where insurance CSRs are thriving—where client satisfaction is high and turnover is low—aren't working harder. They're eliminating the information hunting that makes every "quick question" take 15 minutes.

Lisa still works hard. She still handles high call volume and demanding clients. But now she spends her time actually serving customers instead of hunting through carrier portals and PDFs.

Her clients get immediate answers instead of callbacks. They feel taken care of instead of tolerated. And Lisa feels like she's actually good at her job—because she finally has the tools to BE good at it.

Ready to turn your insurance CSRs into customer service superstars? DM Quentin on LinkedIn to chat more.

FAQ: Insurance CSR

What does CSR mean in insurance?

CSR stands for Customer Service Representative. An insurance CSR works inside an agency to assist clients with policy questions, documentation requests, certificates of insurance, billing issues, and policy changes.

Do Insurance CSRs Need Certifications?

Many insurance customer service representatives (CSRs) pursue professional designations to deepen their expertise.

One of the most common is the CISR (Certified Insurance Service Representative) designation, which focuses on:

policy coverage knowledge

client service best practices

risk management fundamentals

agency operations

While certification isn't required to become an insurance CSR, agencies often value CSRs who pursue continuing education because it improves the quality of service they provide to clients.

What is the difference between an insurance agent and an insurance CSR?

An insurance agent or producer focuses primarily on selling insurance policies and generating new business. An insurance CSR focuses on servicing existing clients, answering questions, and handling day-to-day policy requests.

What skills are important for an insurance CSR?

Successful insurance CSRs typically have strong:

customer service skills

attention to detail

insurance coverage knowledge

communication abilities

organizational skills

Is insurance CSR a good career?

Yes. The insurance CSR role is often the foundation of a long-term career in the insurance industry, with many CSRs advancing into positions such as:

account manager

producer

agency operations manager