Insurance Customer Relationship Management: Why Client Executives Are Stuck in Spreadsheets

What Is Insurance Customer Relationship Management?

Insurance customer relationship management (CRM) refers to the systems and processes insurance agencies use to track client interactions, manage policy relationships, and maintain long-term customer loyalty. At its core, insurance CRM helps agencies centralize client information, policy data, communication history, and renewal timelines so teams can provide proactive service instead of reactive support.

In a modern insurance agency, customer relationship management goes far beyond storing contact details. It enables brokers and client executives to:

Monitor portfolio health

Track policy renewals

Analyze loss history

Identify cross-sell opportunities

Deliver proactive risk advice

When implemented well, insurance customer relationship management transforms agents from transaction processors into strategic advisors, strengthening client relationships and improving retention.

But in many agencies, the reality looks very different. Which brings us to David.

Behind the Desk: A Day in the Life of a Client Executive

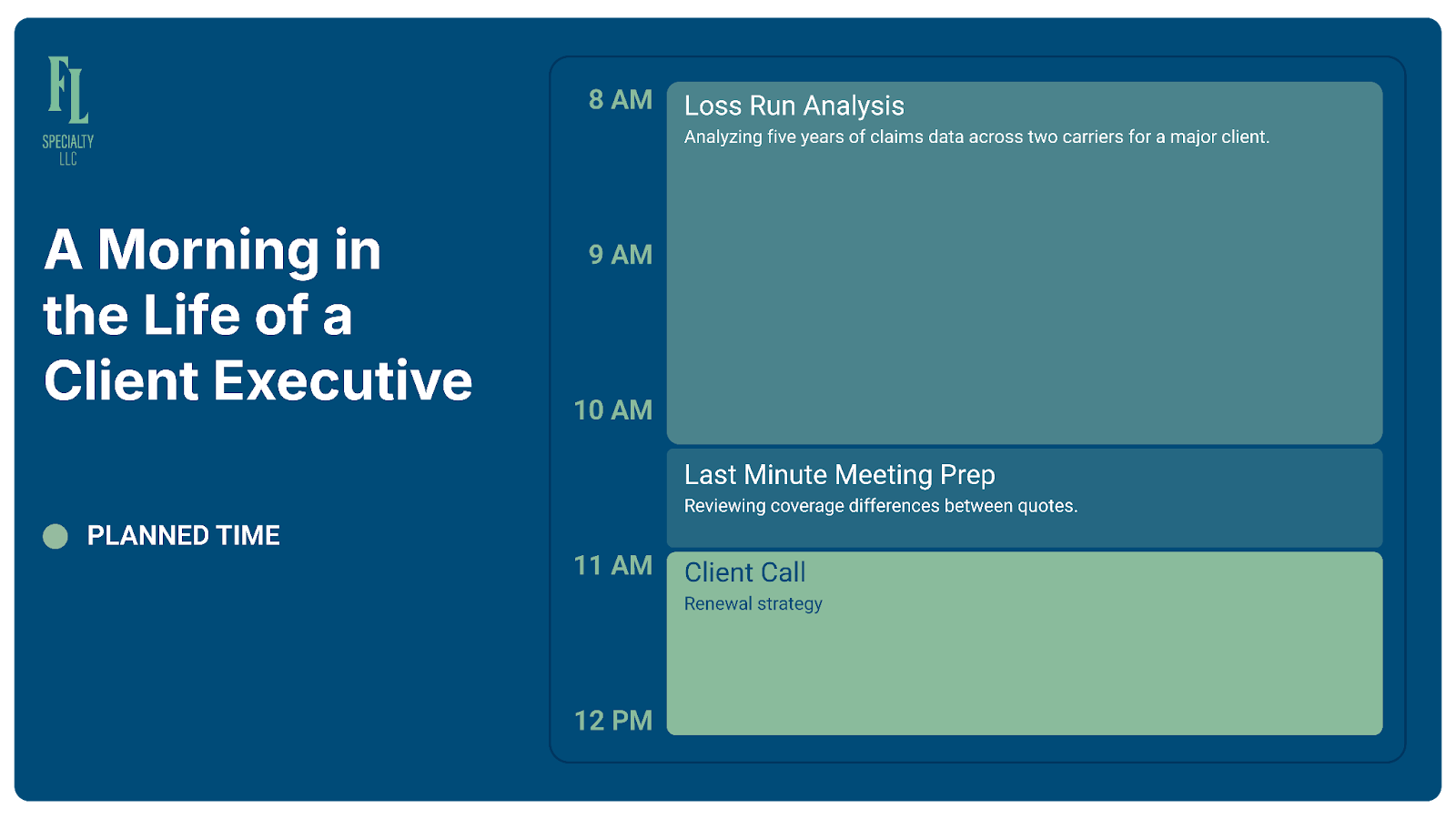

It's 7:45 AM on a Monday, and David is reviewing his book of business over coffee. He's responsible for $2.3M in annual revenue across 47 client accounts. Twelve of them renew in the next 60 days. He's trying to figure out which ones need immediate attention, which ones are solid, and which ones might be at risk of walking.

The problem is, he's doing this based on gut feel and scattered notes rather than actual data. He knows Johnson Manufacturing had some claims last year, but how bad was it really? Peterson Logistics seemed happy at their last meeting, but their renewal is in three weeks and he hasn't analyzed the loss runs yet. Williams Construction has been with the agency for nine years—are they happy or just inertia?

David should be the strategic advisor his clients rely on. Instead, he's flying blind on his own portfolio health until problems surface, then scrambling to fix them under deadline pressure.

If you're a client executive, you know this feeling. You own the relationship. You're measured on retention and revenue growth. But you're spending your time building renewal comparisons and decoding loss runs instead of actually advising clients—and when you lose an account, it's often because "the other broker seemed more on top of things."

This is the hidden problem with insurance customer relationship management inside many agencies: client executives are responsible for relationships, but most of their time is spent doing manual analysis instead of managing those relationships.

The Morning: When Strategy Becomes Scrambling (8 AM - 12 PM)

At 8:15 AM, David's phone rings. It's his largest client—a manufacturing company generating $187K in annual revenue. Their renewal is in three weeks and David sent them the incumbent carrier's renewal quote yesterday: 24% increase.

"David, we need to talk about this. This is unsustainable. What's driving this increase? What are our options?"

David should have had this analysis ready before he sent the quote. The loss runs have been available in the carrier portal for weeks, but he hasn't had time to analyze them yet. He sent the renewal quote to the client without fully understanding what's behind the increase or having alternative options ready.

"Let me pull your loss history and analyze what's driving this increase, then I'll start marketing to other carriers immediately. I'll get back to you this afternoon with a clear picture," David says.

After he hangs up, he logs into the carrier portal and downloads the loss runs—five years of claims data across two carriers. He should have reviewed this a month ago when renewal season started. Instead, he's scrambling now with the client already upset and questioning whether he's on top of their account.

He starts building a spreadsheet to make sense of it—manually typing claim dates, types, amounts incurred, amounts paid. He needs to calculate frequency trends, identify severity issues, figure out what pattern the carrier saw that triggered the 24% increase before he can intelligently market this to other carriers.

An hour later, he's made it through about half the data.

His account manager calls.

"The Williams Construction renewal quote just came in. Want me to start working on a comparison with the incumbent?"

"Yes, please," David says, knowing this means he'll need to review a detailed comparison later today and prepare for a client meeting.

At 10:00 AM, David is still typing claim data from the manufacturing client's loss runs.

This is mind-numbing work—and it's exactly the type of work that insurance customer relationship management systems are supposed to eliminate.

The Afternoon: Fighting Fires Instead of Building Strategy (12 PM - 6 PM)

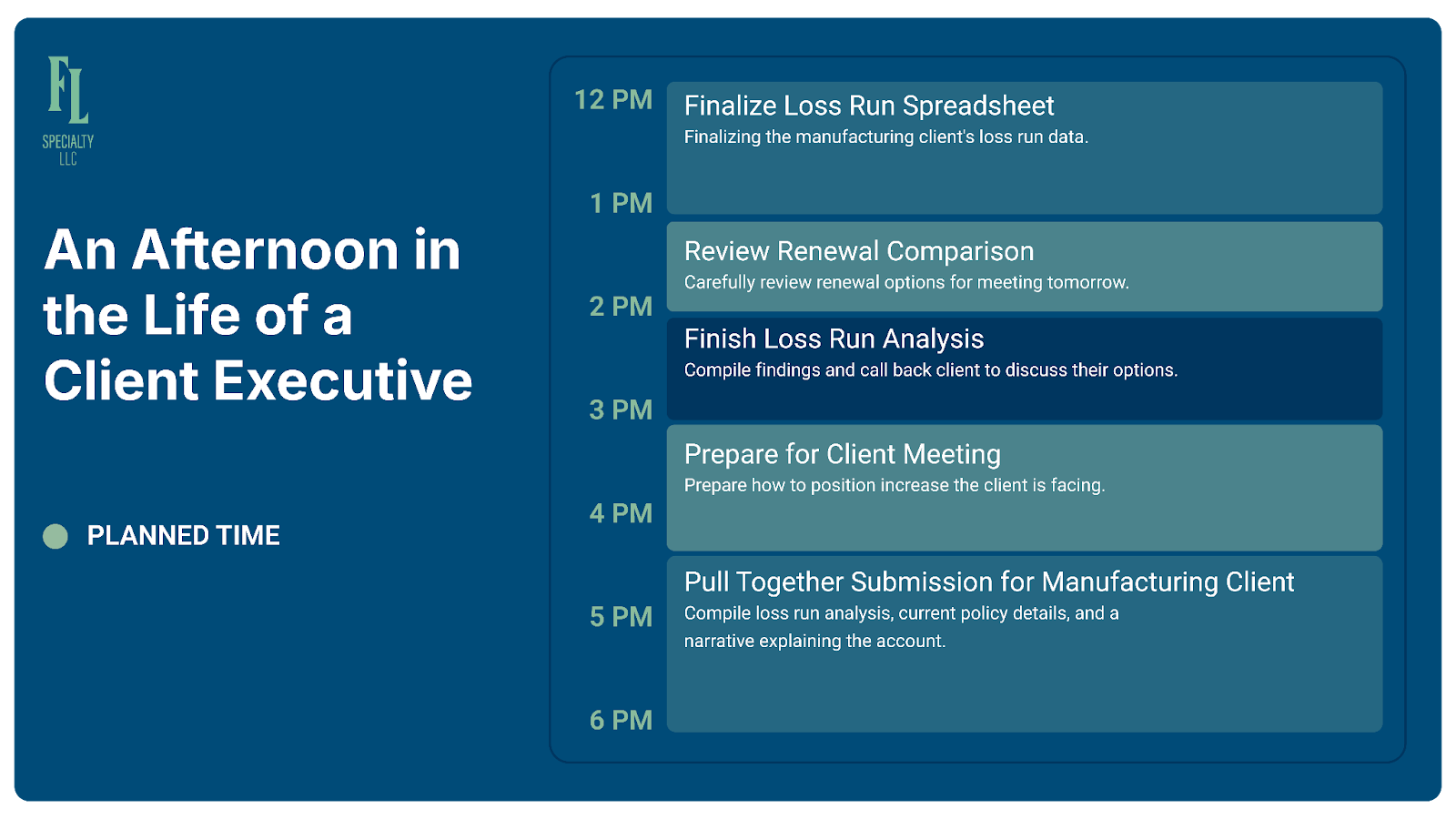

At 1:00 PM, David finally finishes entering the manufacturing client's loss run data. Now he needs to analyze it—calculate frequency by year, identify trends, and figure out what story to tell both the client and potential alternative carriers.

At 2:30 PM, David gets an email from a client he hasn't heard from in months:

"Hi David, just wanted to let you know we've decided to move our insurance to another broker."

David stares at the email. This was a $43K account. He didn't see it coming.

The truth is, he hasn't done a comprehensive review of that account in over a year. He didn't know they were unhappy because he never had time to proactively check in.

Instead of managing relationships, he's been buried in spreadsheets.

At 6:30 PM, David leaves the office. He handled two urgent renewal situations. He lost an account he didn't see coming. And he didn't make any progress on the proactive account management that's supposed to be his primary job.

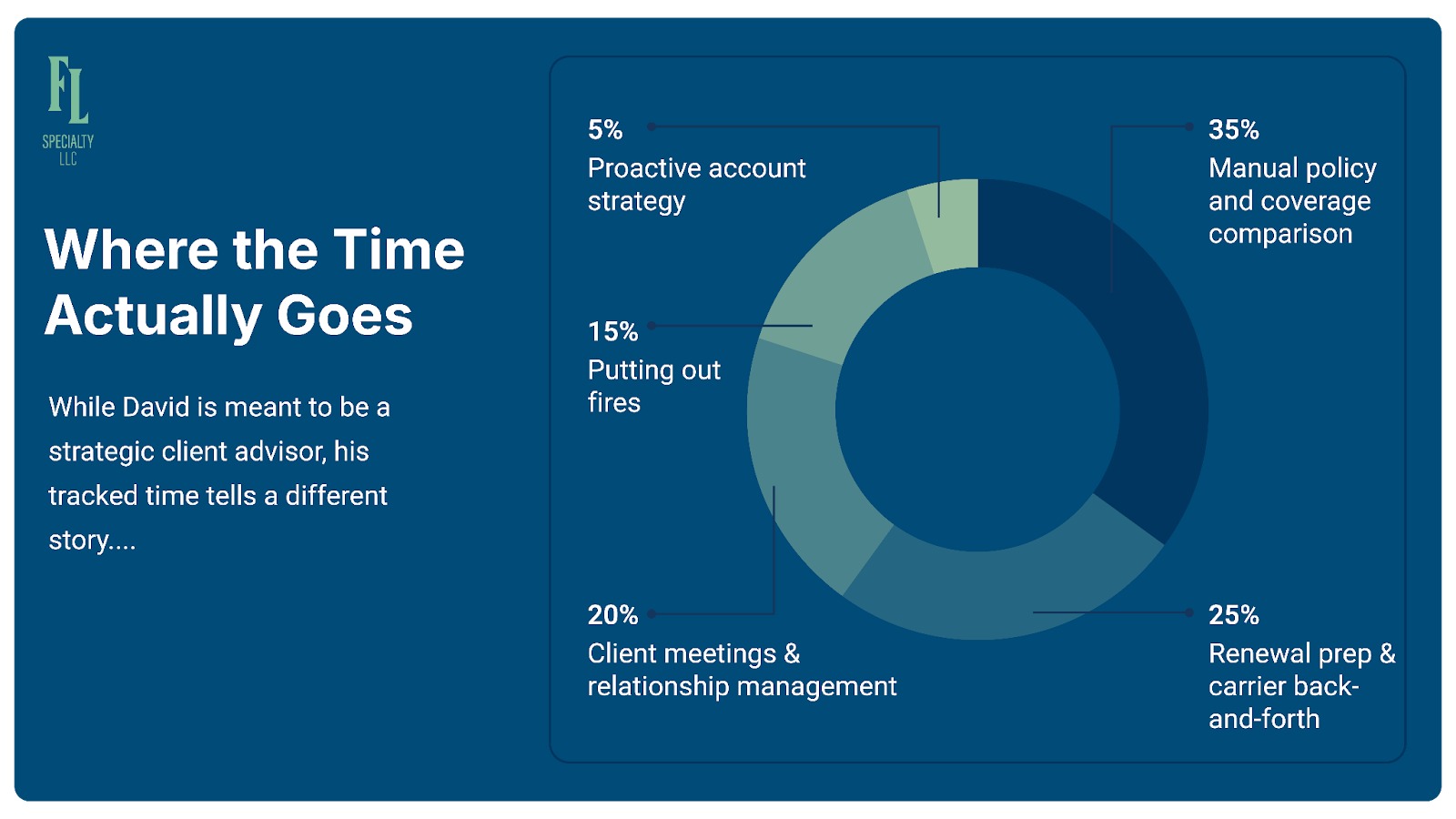

Where the Time Actually Goes

David is supposed to be responsible for insurance customer relationship management across his entire book of business.

But if he tracked his time honestly:

35% – Manual policy and coverage comparison: Extracting data from PDFs, building spreadsheets, trying to create apples-to-apples comparisons for client renewal meetings.

25% – Renewal preparation and carrier back-and-forth: Scrambling to gather information, analyzing loss runs manually, preparing submissions—reactive work, not strategic planning.

20% – Client meetings and relationship management: Less than it should be, and often he's showing up unprepared.

15% – Putting out fires and handling escalations: Clients with problems, claims issues, last-minute coverage questions.

5% – Proactive account strategy and portfolio planning: Quarterly business reviews, identifying at-risk accounts, spotting cross-sell opportunities, strategic relationship building.

That last number—5%—is the killer. David spends one hour per week on the activity that actually drives retention and organic growth. The rest of his time is consumed by manual analytical work that makes him look reactive instead of strategic.

Why Insurance Customer Relationship Management Matters for Agencies

For insurance agencies, customer relationships are the foundation of long-term revenue.

Retaining an existing client is significantly less expensive than acquiring a new one, which is why strong insurance customer relationship management practices are critical for agency growth.

Effective CRM strategies enable agencies to:

Improve Client Retention

Centralized client data and historical insights help agencies identify risks to relationships before renewal time.

Deliver Proactive Service

Tracking interactions, claims trends, and policy changes allows advisors to anticipate issues before they become problems.

Identify Growth Opportunities

CRM data helps reveal cross-sell opportunities and evolving coverage needs.

Reduce Administrative Work

Automation removes manual tasks so producers and account executives can focus on client relationships.

The challenge is that many agencies technically have CRM tools—but the workflows supporting them are still manual.

Which is exactly what David experiences every day.

Key Capabilities of Insurance Customer Relationship Management

A strong insurance customer relationship management strategy typically includes several core capabilities:

Centralized Client Data

All policy details, claims history, communication records, and documents are stored in one place.

Portfolio-Level Visibility

Agencies can monitor the health of their entire book of business and identify at-risk accounts.

Workflow Automation

CRM platforms automate follow-ups, renewal preparation, and reporting.

Data-Driven Insights

Analytics help agencies identify claim trends, coverage gaps, and growth opportunities.

These capabilities allow agencies to move from reactive account servicing to proactive client relationship management.

But without the right workflows, even the best CRM system falls short.

The Technology Solution: Becoming the Strategic Advisor

Strong insurance customer relationship management doesn’t just store client contact information—it helps client executives understand risk trends, renewal dynamics, and portfolio health before problems appear.

The difference between reactive and proactive relationship management often comes down to how much time agencies spend on manual analysis.

The Old Way: Analyzing Loss Runs for Renewals

Manufacturing client's renewal has a 24% increase. David needs to understand why. His process looks like this:

Download loss runs from carrier portal

Open PDFs—14 pages across two carriers

Build Excel spreadsheet

Manually type claim data: date, type, incurred, paid, status

Fix errors and duplicates

Categorize by type

Calculate frequency by year

Calculate severity trends

Identify patterns

Build narrative summary

Total time: 3+ hours to understand one client's loss history. By the time David has answers, the client is already frustrated with the wait.

The New Way: Loss Run Analyzer

David uploads the loss run PDFs. The tool automatically:

Extracts claim data regardless of carrier format

Categorizes claims by type

Calculates claim frequency and severity trends

Identifies patterns in the loss history

Highlights concerning signals

Total time: 8 minutes from upload to complete understanding.

Now David can call the client back within an hour with clear answers.

Even more importantly, he can run this analysis weeks before renewal, which is how strong insurance customer relationship management actually works in practice—anticipating issues before they surprise clients.

Instead of reacting to problems, David becomes the advisor who sees them coming.

The Old Way: Preparing Renewal Comparisons

Williams Construction renewal includes incumbent policy and two competing quotes. David's preparation process looks like this.

Download three policies

Build comparison spreadsheet

Search incumbent PDF for coverage details

Search Quote 1—different format

Search Quote 2—package policy structure

Extract and compare limits across all coverages

Identify coverage differences and gaps

Format for client presentation

Total time: 3.5+ hours to prepare for one renewal meeting.

David walks into the meeting with a comparison.

But because he spent the entire afternoon building the spreadsheet, he hasn't had time to think strategically about the client's business or prepare recommendations.

From the client’s perspective, the broker is simply delivering quotes—not advising.

This is another place where insurance customer relationship management suffers when manual workflows dominate.

The New Way: Quote & Policy Comparison Tool

Now David uploads the incumbent policy and two competing quotes into an automated comparison tool.

The system:

extracts coverage limits automatically

identifies deductibles and endorsements

maps policies side-by-side

highlights coverage gaps

flags meaningful differences

It produces a client-ready comparison summary.

Total time: 15 minutes including review.

Now David can spend the remaining time doing the work that actually strengthens client relationships:

researching the client’s industry trends

identifying emerging risks

preparing strategic coverage recommendations

Instead of showing up with a spreadsheet, he shows up with insight.

That's the difference between administrative work and real insurance customer relationship management.

The Old Way: Portfolio Management

At the portfolio level, David's process used to look like this:

Manually review renewal dates in spreadsheet

Try to remember which accounts had claims (unreliable memory)

Dig through files for accounts that might be at risk

Still miss warning signs

That's exactly how the Henderson account slipped away.

Without visibility across the portfolio, client executives end up managing relationships reactively instead of strategically.

The New Way: Data-Driven Portfolio Strategy

When loss run analysis and policy comparison take minutes instead of hours, the entire approach to insurance customer relationship management changes.

David can now:

analyze loss trends across every account quarterly

identify deteriorating loss ratios 6–9 months before renewal

schedule proactive risk management discussions

identify accounts with cross-sell opportunities

segment his book by health status:

Green — stable accounts

Yellow — accounts needing attention

Red — at-risk relationships

Instead of reacting to problems, David manages his portfolio proactively.

That’s what modern insurance customer relationship management should enable.

What Better Actually Looks Like

Six months later, David’s day looks very different.

At 7:45 AM, he’s reviewing his book—but now he’s looking at real data. He’s already analyzed the loss trends for every account renewing in the next 90 days, so he knows which clients are stable, which need attention, and which accounts require early marketing.

When his manufacturing client’s renewal comes in with a 24% increase, David isn’t surprised. He ran the loss analysis weeks earlier and already discussed the trends with the client. When he sends the renewal quote, it includes context, alternatives, and recommendations—not just a number that sparks panic.

At the Williams Construction meeting, he spends minutes reviewing the policy comparison and the rest of the time discussing their expansion plans, cyber exposure, and coverage strategy.

Later that afternoon, David runs his quarterly portfolio review, identifying at-risk accounts and scheduling proactive conversations before renewal.

Six months later, retention is 96% (up from 89%) and organic growth is 12% (up from 4%).

David isn’t working longer hours—he’s just spending them advising clients instead of building spreadsheets.

The Bottom Line for Client Executives

True insurance customer relationship management requires time for strategic thinking, proactive conversations, and relationship building.

But when client executives spend most of their week doing manual analysis, those relationships suffer.

The accounts that leave often don't do so because of price or coverage.

They leave because another broker looked more proactive, more prepared, and more strategic.

The math is simple: Every hour spent building spreadsheets is an hour not spent advising clients. David still manages a large book. But now he spends his time where it matters—relationships, strategy, and growth.

Ready to spend your days advising instead of analyzing? DM Quentin on LinkedIn to chat more.

Insurance Customer Relationship Management FAQs

What is insurance customer relationship management?

Insurance customer relationship management refers to the systems and processes insurance agencies use to manage client relationships, track policy information, and improve customer retention.

Why is CRM important in insurance?

CRM systems help insurance agencies centralize client data, automate workflows, and improve service quality, enabling advisors to provide proactive guidance.

What features should an insurance CRM include?

Most insurance CRM platforms include:

Client contact and policy management

Renewal tracking

Claims and loss history analysis

Automated follow-ups

Reporting and analytics