Behind the Desk: A Day in the Life of an Insurance Producer

It's 6:45 AM and Jennifer, an experienced insurance producer, is already at her desk—not because she's an early bird, but because it's the only quiet time she'll get all day.

She's got her prospecting list pulled up, 23 businesses she's researched who should be ideal fits for the agency. She's blocked out 7-9 AM for outreach calls. She's caffeinated, focused, and ready to do what she was actually hired to do: sell.

Her phone buzzes at 7:12 AM. Text from the account manager: "Client needs quote comparison for renewal by EOD—can you help? I'm underwater."

There goes the morning.

If you’re an insurance producer, you know this story by heart. You were hired to hunt—to bring in new business, grow your book, and build revenue. Your compensation plan is built around production. But instead of selling, you’re buried in renewals, policy analysis, and manual comparisons—not because you want to be, but because if you don’t step in, your retention suffers and your revenue walks out the door.

In this article, we’ll break down what insurance producers do, where their time really goes, and why so many producers struggle to balance new business growth with client retention. We’ll also show how modern technology is changing the role—eliminating hours of manual policy comparisons, quote analysis, and loss run reviews—so insurance producers can spend more time doing what they were hired to do: sell.

What does an insurance producer actually do?

An insurance producer is a licensed professional authorized to sell, solicit, and negotiate insurance policies. In most states, “producer” is the official licensing term and includes both agents and brokers.

In practice, insurance producers are expected to:

Prospect and generate new business

Advise clients on coverage options

Place policies with carriers

Retain and grow their book of business

The problem? The modern insurance producer’s day rarely reflects that job description. Just take a look at Jennifer’s day.

The Morning That Never Was (6:45 AM - 12 PM)

Jennifer stares at her prospecting list for another 30 seconds, knowing she’s about to abandon it. She texts back: “Which client?”

It’s one of her accounts—a $38K annual revenue manufacturing client she brought in two years ago. The incumbent carrier came in 22% higher at renewal. She has quotes from three other markets, but they’re all formatted differently. The client called yesterday and said they need a clear comparison by end of day or they’re “bringing in another broker.”

This is Jennifer’s problem to solve. It’s her client. Her revenue. And if it walks, it hits her commission and her retention metrics directly.

By 7:30 AM, she’s downloaded all four policies. One is a bundled package policy. One splits general liability, property, and auto into separate documents. Another has endorsements scattered across 47 pages.

Jennifer opens Excel.

She hunts through PDFs. Copies coverage limits. Tracks down endorsements that quietly modify aggregates. Compares blanket limits against specific location limits using different valuation methods.

At 9:15 AM, she’s still building the spreadsheet. Her prospecting window is gone. Her phone has three missed calls from prospects she researched last week—prospects who are likely calling competitors now.

By 11:30 AM, she finally walks the client through a clean comparison. She finds coverage gaps that would’ve been disasters. She saves the account.

But she’s burned four and a half hours on retention work—time she should’ve spent selling.

Her prospecting list is still untouched.

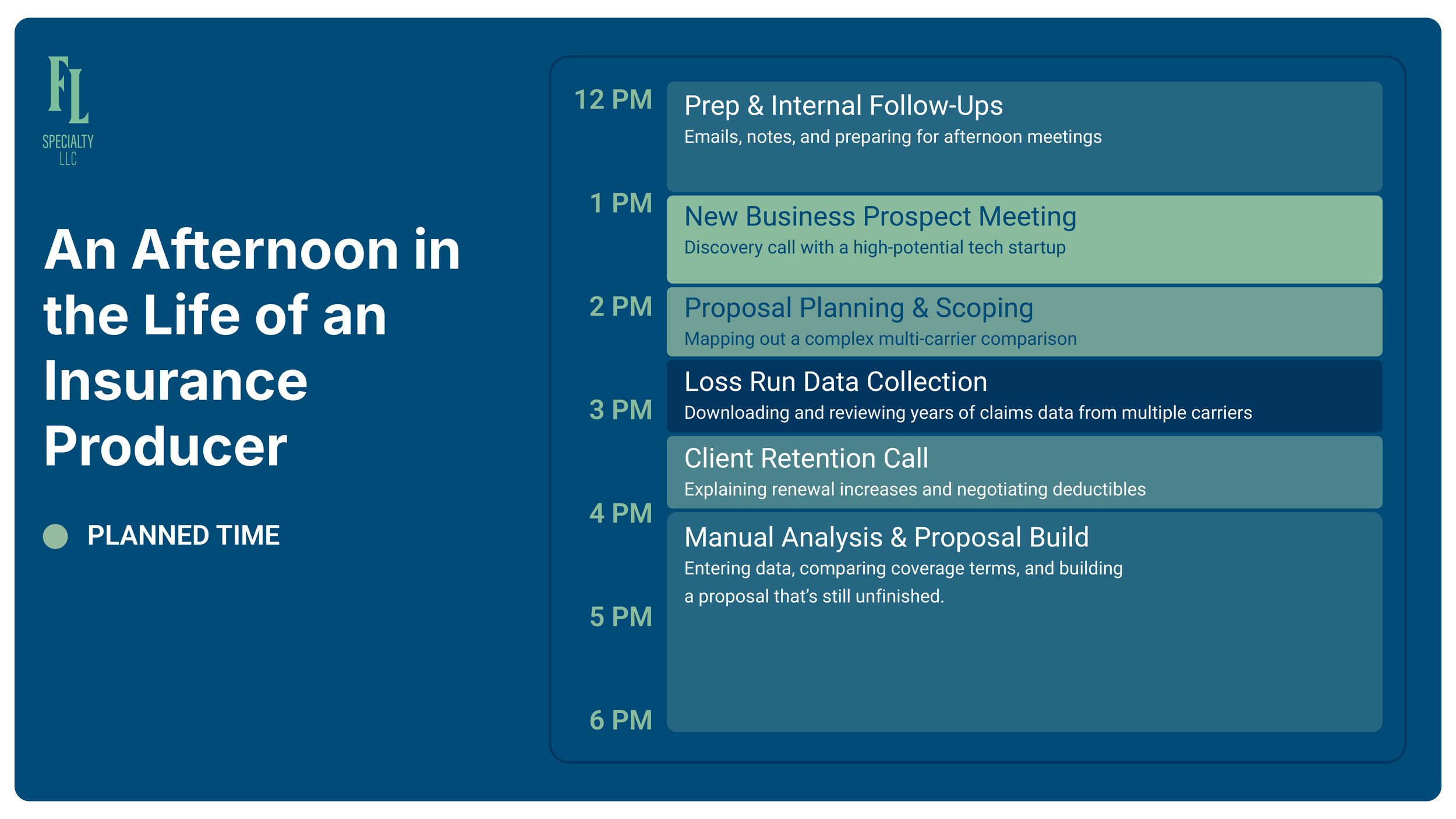

The Afternoon Grind: When Your Own Deals Need You (12 PM - 6 PM)

At 1 PM, Jennifer meets with a tech startup prospect—exactly the kind of business she wants. The meeting goes great. They want a proposal by Friday comparing three carriers with different coverage approaches.

But Jennifer knows what that means.

To build the proposal, she’ll need to extract coverage details from massive PDFs, compare terms side-by-side, and build a professional presentation. That’s 4+ hours of analytical work for a single prospect.

At 2:15 PM, another client calls—a contractor generating $22K annually. Their renewal came in 40% higher. They’re furious. They want answers. They want options.

Jennifer pulls five years of loss runs from two carrier portals. The formats are inconsistent and messy. She knows what’s coming: hours of manual data entry, categorization, and trend analysis.

At 3 PM, her manufacturing client calls again. Another 45 minutes negotiating deductibles.

By 6 PM, Jennifer is still at her desk, staring at a half-finished proposal. Her prospecting list—the one she started the day excited about—never got touched.

Where the Time Actually Goes

Jennifer's supposed to be a producer. Her job description says: "Generate new business revenue through prospecting, relationship building, and consultative selling." Her compensation plan rewards new client acquisition and book growth.

But if she tracked her time honestly for a month, here's what she'd find:

40% – Manual quote and policy comparison: Building spreadsheets, extracting data from PDFs, cross-referencing coverage terms for both prospects and existing clients.

20% – Data entry and administrative work: Updating the CRM, chasing down paperwork, processing endorsements.

20% – Actual client conversations and relationship building: The part of the job she's good at and enjoys.

15% – Retention and renewal support for her own book: Coverage questions, renewal issues, loss analysis—necessary work that doesn't count toward her new business goals.

5% – Strategic prospecting and new business development: The thing she was hired to do.

Jennifer spends one hour per week on the activity that determines whether she hits her goals and earns the commission she needs to live on.

The problem isn't that Jennifer is lazy. She's caught in an impossible squeeze: she needs to protect her existing revenue (retention) while simultaneously growing new revenue (production). Both suffer because the analytical work—comparing policies, analyzing loss runs—eats up the hours she should be spending on strategic selling.

The Technology Solution: Reclaiming the Selling Time

The Old Way: Comparing Renewal Quotes

Jennifer's $38K manufacturing client needs that renewal comparison:

Download incumbent policy and three competing quotes (5 minutes)

Search through 67-page PDF for specific coverages (20 minutes)

Hunt for endorsements that modify coverage (15 minutes)

Copy information into Excel (10 minutes)

Repeat for second carrier with different format (25 minutes)

Repeat for third carrier with completely different structure (30 minutes)

Build comparison table (45 minutes)

Realize she missed something, go back to PDFs (20 minutes)

Format for the client (30 minutes)

Total time: 3+ hours to keep one client from walking. With five renewals hitting this month, that's 15+ hours on retention work instead of prospecting.

The New Way: Quote & Policy Comparison Tool

Jennifer uploads the incumbent and three competing quotes. The tool:

Automatically extracts all coverage limits, deductibles, and endorsements

Creates a side-by-side comparison highlighting key differences

Flags coverage gaps where competing quotes fall short

Generates a client-ready report

Total time: 12 minutes.

Jennifer saves the account and gets back to prospecting before her coffee gets cold. That's 3+ hours reclaimed for revenue-generating activity.

The Old Way: Building Prospect Proposals

When the tech startup wants a three-carrier comparison:

Download three massive PDFs (total 198 pages)

Search first PDF for cyber coverage limits (20 minutes)

Find coverage terms in endorsement on page 38 (10 minutes)

Copy into Excel (10 minutes)

Repeat for second carrier (25 minutes)

Repeat for third carrier with different format (30 minutes)

Build comparison table (45 minutes)

Format into professional presentation (40 minutes)

Write narrative explaining recommendations (30 minutes)

Total time: 4+ hours per proposal. With three active prospects, that's 12+ hours per week on data extraction instead of selling.

While Jennifer is buried in PDFs, her competitor with better tools already delivered a polished proposal.

The New Way: Quote & Policy Comparison Tool

Jennifer uploads the three carrier quotes. The tool creates a complete comparison in 12 minutes. Now she focuses on the part that actually wins deals—explaining why certain coverage approaches make sense for this specific client's situation. She's selling strategic value, not just extracting data.

The Old Way: Analyzing Loss Runs

That contractor with the 40% renewal increase? Jennifer needs to understand their loss history:

Download loss runs (5 minutes)

Manually type claim data into Excel for 5 years (90 minutes)

Fix errors (15 minutes)

Categorize by type (20 minutes)

Calculate frequency and severity (35 minutes)

Try to identify patterns (30 minutes)

Build summary (20 minutes)

Total time: 3+ hours of data entry. And she's still not certain she identified the real issue.

The New Way: Loss Run Analyzer

Jennifer uploads the loss run PDF. The tool:

Extracts all claim data regardless of carrier format

Categorizes by type, calculates trends

Identifies patterns: "8 claims in past 3 years vs. 2 in prior period. Two large GL claims totaling $87K significantly elevated total incurred."

Generates visual charts and summary

Total time: 8 minutes.

Now Jennifer can call her client back the same day with actual answers. She knows exactly why the carrier increased the premium and can have a strategic conversation about solutions. When she markets to other carriers, she's armed with a data-driven story that gives her a real shot at competitive quotes.

What Better Actually Looks Like

Six months later, Jennifer's days look different.

It's 6:45 AM and she's at her desk with her prospecting list. When that renewal comparison request comes in at 7:12, Jennifer uploads the policies, reviews the output in 10 minutes, and sends back a complete analysis before 7:30 AM. The client is saved. Jennifer is back to prospecting.

She makes 12 calls before 9 AM, connects with four people, and schedules a meeting with a promising prospect.

At 10 AM, she meets with a prospect who's ready to see options. She requested quotes last week and spent 15 minutes yesterday generating the comparison. This morning she researched the prospect's industry challenges and prepared strategic talking points. She walks into the meeting confident, prepared, and focused on solving business problems—not scrambling to finish a spreadsheet.

The prospect asks detailed coverage questions. Jennifer has clear answers immediately. She's not reading off a spreadsheet—she's explaining why certain approaches make sense for their risk profile. The prospect is impressed and asks for a follow-up with their CFO.

After lunch, that contractor calls about their loss history. But Jennifer already ran the analyzer. She knows exactly what's in the loss runs and what the path forward looks like. The conversation takes 20 minutes instead of "let me get back to you tomorrow." She saves the account and the client is grateful for how quickly she handled it.

That tech startup proposal? She finished it yesterday in under an hour. This morning she got the response: they want to move forward. Jennifer just closed a $47K new revenue account—one she almost wouldn't have had time to pursue properly before.

At 5:30 PM, she leaves on time. Her prospecting list has check marks next to 15 names. She's moved three deals forward. She's handled two urgent renewals without derailing her day. And she feels like she actually did the job she was hired to do.

Her numbers the next month tell the story: 40% more new revenue than her previous quarter—not because she's working harder, but because she's actually spending time selling instead of building spreadsheets. Her retention is up too, because she can respond to renewal challenges quickly and professionally.

She's not choosing between retention and growth anymore. She's doing both.

The Bottom Line for Producers

You were hired to sell—not to format PDFs and build spreadsheets.

Every hour an insurance producer spends on manual analysis is an hour not spent prospecting, advising, or closing deals. Agencies with top-performing producers aren’t asking them to work more—they’re eliminating the analytical grunt work that keeps salespeople chained to their desks.

When producers reclaim their time, both growth and retention improve.

Ready to spend your days selling instead of formatting? DM Quentin on LinkedIn to chat more.

Frequently Asked Questions

What does an insurance producer actually do?

An insurance producer is responsible for generating revenue for an insurance agency by prospecting for new clients, placing coverage with carriers, and retaining existing accounts. While the role is sales-driven, producers are often pulled into renewals, quote comparisons, loss analysis, and client problem-solving—especially on accounts they personally sold and manage.

How do insurance producers spend most of their time?

Although insurance producers are hired to sell, much of their time is spent on manual work: comparing policies, extracting coverage details from PDFs, reviewing loss runs, and building spreadsheets for clients. This administrative and analytical work can consume the majority of the week, leaving limited time for strategic prospecting and sales conversations.

How can insurance producers increase production without working more hours?

The most effective way for insurance producers to increase production is by eliminating manual analytical work. Tools that automate quote comparisons, policy analysis, and loss run reviews free up hours each week—allowing producers to focus on prospecting, client meetings, and closing deals instead of building spreadsheets.